Why Traders Are Refusing To Give Up On The Idea Of A March Fed Rate-Cut

Authored by Ven Ram, Bloomberg cross-asset strategist,

Despite pushback from Fed officials, the markets are growing in conviction that an interest-rate cut is possible as early as March.

History is on the side of markets.

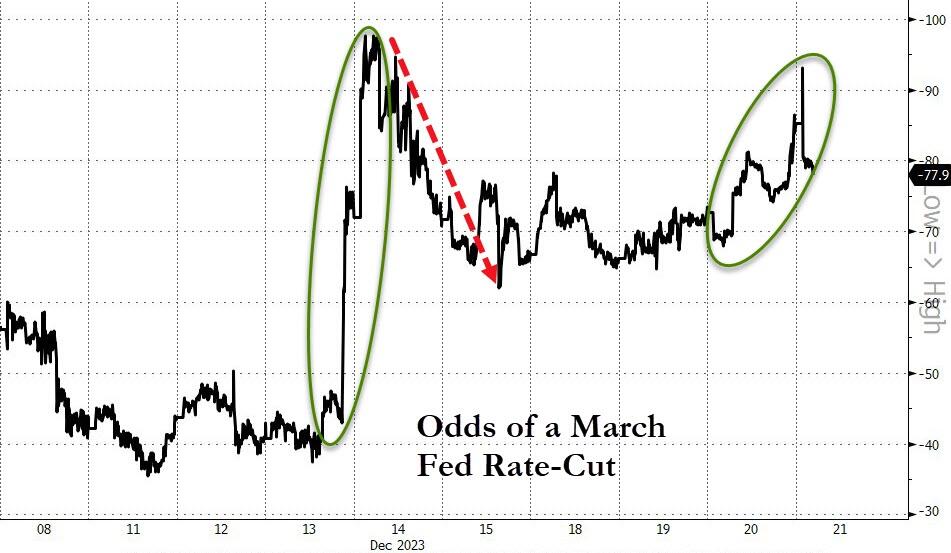

Interest-rate traders, who were ascribing almost a 100% chance of a 25-basis point cut in March after last week’s dot plot, had trimmed their assessment to some 60% by the start of this week as Fed officials from John Williams to Loretta Mester to Raphael Bostic all pushed back on the notion of an early reduction.

Traders have since raised that possibility again, this time to around 90%.

{kind=link}

What gives?

Well, the median time for the Fed to go from a hike to a cut has been 231 days in data going back almost three decades.

{kind=link}

Given that we got the last rate increase in July, the Fed’s March meeting will have won history’s sanctification.

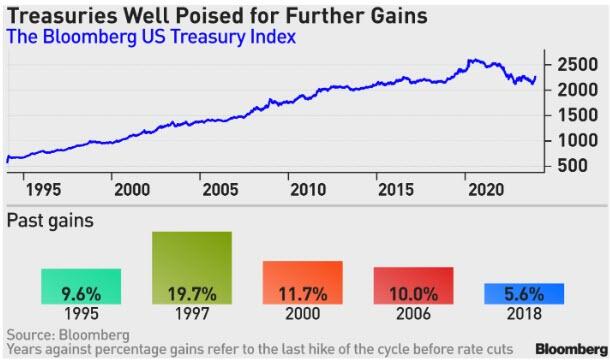

That’s not all: the Bloomberg Treasury Index is bound to recover to levels last seen when the Fed started raising rates.

The Bloomberg Treasury Index has made hay in the interregnum between tightening and loosening cycles, having gained unfailingly in each of the past five iterations.

Gains between the end of 2018 when the Fed ended raising rates and August 2019 when it cut rates were about 5.6%, the least historically.

Assuming a conservative reprisal of those gains, the index is on track to re-claim around 2,352, last seen around the time when the Fed started tightening rates in this cycle.

{kind=link}

The Fed’s latest dot plot showed that policymakers were willing to reduce the funds rate by 75 basis points next year, spurring a 2% rally in the Bloomberg Treasury Index last week, its best performance since the early days of the pandemic.

The dovish dot plot may have stemmed from the Fed’s conviction that rates needn’t be as restrictive in the face of headline inflation that has halved to 3.1% this year.

{kind=link}

However, core inflation remains sticky at 4%, posing a risk to the market’s pricing.

Denials by Fed Speakers notwithstanding, should the Fed be persuaded otherwise by continued progress in disinflation to cut rates, two-year Treasury yields may slump below 4% while the pace of gains in 10-year Treasuries slows, causing the yield curve to re-steepen.

Tyler Durden

Thu, 12/21/2023 – 10:25