The Red Sea Crisis Has Created Winners And Losers: The US Is A Loser, The Winners Again Are China And Russia

By Benjamin Picton of Rabobank

Outside Reversal

US stocks ended the session down bad yesterday after initially rallying on rate cut bets that had carried over from Europe. The S&P500 printed an outside reversal candlestick as it fell by (almost) 1.5%. This was despite another sharp fall in bond yields which saw the US 2-year down 11bps to 4.335% and the 10-year down 8bps to 3.85% after UK CPI recorded a big downside surprise to fall from 4.6% in October to 3.9% in October (below even the most optimistic forecast on the Bloomberg survey). Oil prices didn’t move much. Brent closed at $79.19/bbl, gold continued its consolidation above the $2000/ounce technical level and the VIX index rose by more than 9% (!) just one week after it threatened to take out the January 2020 lows.

So what gives? Is this the end of the melt-up in stocks that has been running hot since the Fed signaled a pivot last week? If it is, it seems strange that it would happen on a day when yields fell so sharply. The textbooks tell us that we SHOULD expect higher bond prices when stocks fall, but anyone who has traded this market over the last couple of years knows that in reality the correlations there are closer to 1 than they are to -1.

FedEx – a bellwether stock reputedly favored by Alan Greenspan as an indicator of economic activity – led losses by declining more than 12% in the session. This perhaps underscores suggestions that Americans are buying less stuff even as retail turnover figures rise due to higher prices paid.

A possible explanation for the selloff is the issue of the Houthi’s crippling the world’s third busiest (after the Strait of Malacca and the Singapore Strait) shipping lane. The Red Sea handles 12% of global maritime trade and 30% of containerised trade. Given the enormity of the impact of this disruption – and the signalling value of the thus far impotent response from the USA and allies – it would be logical to deduce that stocks are finally starting to price in some margin of safety for the huge geopolitical shock that has now moved from the realm of known risk to realized risk.

But there are signs that markets still don’t get it.If the reversal in stocks a reflection of geopolitical risk premia being priced in, why such small moves in oil and gold? Bloomberg reported on Tuesday that the Red Sea’s importance as a conduit for trade in hydrocarbons has surged by 140% since the Ukraine War rejigged supply chains to see cheap Russian crude flowing East and South to China and India while Europe is left to compete for cargoes from Saudi Arabia and other Middle Eastern origins.

Saudi Arabian crude is similar in composition to Russian product, but interruptions to Red Sea shipping risk rekindling problems experienced earlier in the year when Saudi production cuts forced buyers to substitute for light-sweet crude from the United States. Light-sweet crude yields less diesel in the refining process, which contributed to the big blowout in crack spreads earlier in the year. Perhaps the potential for more expensive diesel is part of the reason why energy-intensive industry was particularly bearish on the outlook in the recent German IFO survey?

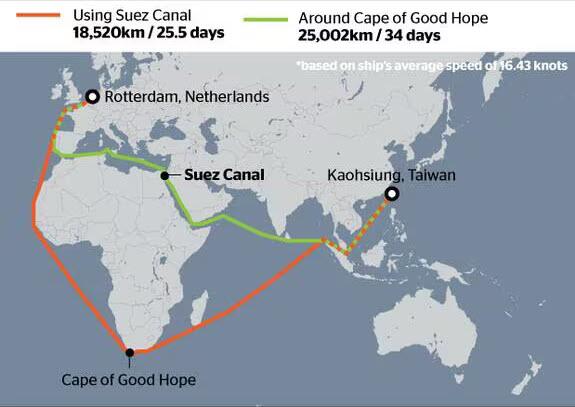

Major shipping companies including Maersk, MSC and Hapag-Lloyd are now diverting shipping away from the Red Sea and instead making the much longer journey around the Cape of Good Hope. This adds 7-15 days to journey times, increases demand for bunker fuel to move those cargoes and reduces the availability of ships and containers as those vessels are tied up for longer to deliver the same volume of cargo. Does anyone remember what happened in 2020 when shipping supply chains got snarled up and containers were piling up in the Port of Los Angeles instead of making their way back to Shanghai? Surely, we should have learned our lesson that global supply chains are fragile and that pushing down on the balloon at one end makes a big difference in pressure at the other end, but the risk premia still doesn’t look priced-in to me.

{kind=link}

Even more concerning than the immediate impact on global supply chains is what the Red Sea crisis says about the United States’ ability to project power and police vital trade routes. The WSJ picked up on this yesterday when they suggested that ‘US Naval Deterrence is Going, Going, Maybe Even Gone’.The cheek of Iranian-backed Houthis in openly targeting US and allied warships with drone and missile attacks – so far without major repercussions – is raising questions about the capacity and willingness of the USA to protect its strategic interests.

This impression that the United States is stretched too thin was reinforced by suggestions that offers of convoy protection were made, but only for US-flagged ships. These offers are rumoured to have been refused by major shippers unless protection was also extended to their foreign-flagged vessels, meaning that European shippers might have tried to strongarm the US Navy into allowing them to free-ride on US military might. Maybe they’re taking notes from NATO?

Concerningly, Marine Tracker data suggests that the launch of Operation Prosperity Guardian has not been sufficient to prevent freight companies from diverting their largest container ships away from the coast of Yemen.The loss of prestige for the global hegemon will not have gone unnoticed by America’s adversaries, who will be emboldened by any signs of weakness.

Adding to the concern has been the lukewarm response of major allies invited to join Operation Prosperity Guardian. Canada committed no ships and opted instead to only send a clutch of staff officers while Australia (an AUKUS ally who fought with the United States in Iraq, Vietnam and Korea) also refused US requests to send a warship to the Red Sea.

The Australian Government claims the refusal was due to a preference to focus on interests in the Asia-Pacific region, but local media has suggested that it is actually because none of Australia’s 7 frigates and 3 air-warfare destroyers are appropriately equipped to deter attacks from cheap Houthi (Iranian) drones for any length of time. If this really is the case, it is an astonishing gap in capability that highlights the extent to which conventional fleets face disruption from small, cheap and agile adversaries. That doesn’t bode well for the security of supply chains elsewhere.

Of course, the situation in the Red Sea has created winners as well as losers. The winners again appear to be Russia and China. The former benefits from further destabilization of Europe, where economic pressures were already splintering solidarity of support for Ukraine. Russia’s Shadow Fleet of oil tankers is also being granted safe passage by the Houthi’s, meaning that they retain access to the most efficient regional supply chain, while Western democracies are forced to take the long war around.

The main alternative shipping route for getting goods from Asia into Europe is to traverse the Bering Strait and the Northern Sea Route, which is shorter even than going through Suez and is becoming increasingly navigable due to the effects of climate change. The only problem is that it is almost entirely Russia-adjacent!

China also benefits from European destabilization and higher energy costs for European manufacturers who are having their lunch eaten by Chinese competitors. Those competitors already enjoy greater scale, greater state support and greater access to cheap Russian energy supplies. Watching the United States divert further naval assets into the Red Sea to underwrite the business-as-usual trade (so far with limited success) must also bring a smile to the face of any PLAN Admiral focused on the goals of Taiwan reunification and Chinese territorial claims in the South China Sea.

So, there are plenty of good reasons for why valuation-stretched equities might print an outside reversal, but the real question is whether this is indeed a turning point, or just a false signal. The price action in the final days leading into Christmas is going to be very interesting indeed.

Tyler Durden

Thu, 12/21/2023 – 11:05