“No Longer In The Bull Camp”

Authored by Peter Tchir via Academy Securities,

The Party is Over

Since the Fed, I have been “torn” on what to do. This weekend, we worried about “snatching defeat from the jaws of victory”. That has followed several weeks of feeling increasingly “reckless” on bullish calls (from Wayne’s World, to Beavis and Butthead).

We started the week mildly bearish yields. That hasn’t done much, and I’m comfortable maintaining or increasing that bearishness.

On equities, maintained a slightly bullish outlook, while favoring laggards, and caveating that by wanting to “buy the dip”. Now I don’t like that and it is time to change that view.

Negative Bias on Equities

Ignoring FedSpeak, inflation, or any talk of “landings” here are some reasons to be bearish equities.

Haven’t liked how equities has been trading past few days. No “oomph” on the moves higher.

Did not like how many people came out blaming 0DTE (zero day to expiration options) for yesterday’s sell-off, but no-one seemed to care that on Dec 14th, 15th and 19th, we saw stocks pop from 2 pm on, into the close. That wasn’t 0DTE? Strikes me as convenient that people are looking for a scapegoat for a sell-off which makes me think people are overly committed to being long a market, with too many rate cuts and too much soft landing enthusiasm baked in.

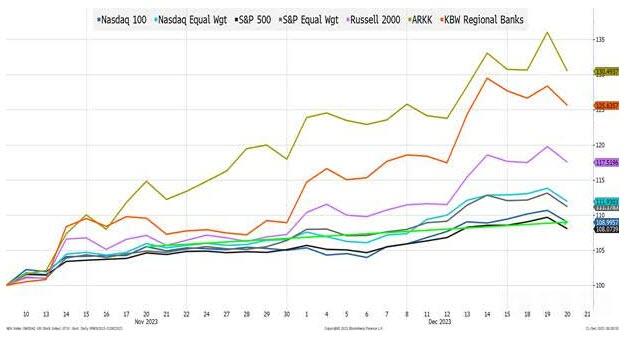

Market cap matters. As we end this year and start another, as people question market cap weighted indices. As investors, many of whom have restrictions on how much of their portfolio any one stock can be, all adjust, I expect some selling pressure that will weigh down the Nasdaq 100. It won’t be “panic” selling, but it is very difficult to absorb the potential dollars being sold if investors reduce their allocation to some of the largest companies. So, if the Nasdaq 100 is weak it will be difficult for equities to do well. The Nasdaq 100 was 16,020 on Nov 20th, and “only” got to 16,221 on Dec 11th, not much movement. It performed well post FOMC, but was trading “tired” for some time.

{kind=link}

Supply. We don’t often talk about “supply” on the equity side of things, but If Wall Street’s hope of a robust IPO calendar is correct, there could be a large amount of new equities that the market has to absorb. Even if the new issues do well, that could weigh on markets. The last time the street was this optimistic about IPO’s was the end of the summer and neither the IPO’s in many cases, nor the market did well with that supply. Something to keep in mind.

Am not a raging bear, but no longer in the bull camp.

Refining the “Laggards”

We’ve been quite generous in what we considered “laggards” – anything from value stocks, to small cap, to Russell 2000, to CRE, to small and mid-size banks, to equal weighted S&P and Nasdaq. Heck we even included “disruptive” tech in the “laggards” camp – as they were not performing up to their typical higher beta performance!

It is time to refine that, and, no pun intended, energy stocks are higher on my list.

Three favorite “lagging” sectors are:

Energy. I don’t like oil a lot here, but this area is ripe for consolidation and as much as we get some “mission statements” from things like COP 28, traditional energy is here to stay for the foreseeable future. Even more importantly, I continue to expect the energy companies of today to be the energy companies of the future as they have the resources and skills to navigate the transition to alternative energy sources.

Commercial Real Estate. The move to lower yields is helpful. The fact that banking fears from early in 2023 have proven to be overdone is useful. Healthy banks, which most are, have time to work with even troubled creditors. That will spread and delay any pay from commercial real estate for the overall market and help CRE companies. Finally, we can go back to calling 2024 as the year of WFO. Whatever the norm was, it has been changing and will continue to change. Not just do the bosses want the workers in, but many of the workers want to be in too (at least a few days a week).

China. I don’t like China longer term and it has been one of the “laggards” that has continue to lag, but I feel forced to bet on some sort of China stimulus package, or “deal” with the U.S. (tariffs, semiconductors and agricultural goods all come to mind) or both!

Some of the other laggards (including foreign stocks more broadly) should outperform the high flyers, but in a down tape (if I’m correct) they may struggle to provide positive returns.

Credit

I think there are better places to express short views – duration and/or equities. But if you are stuck to trading credit, then for the first time in months, I like being slightly bearish on credit.

I like credit better than equities or duration, and I’ve been on a “barbell” approach:

High quality credit (let’s call it BBB+ and above, which might be a bit generous, but it is the holiday season) should do well. They, by and large did a great job locking in “lower for longer” and should benefit from what I think will be a trend of overweighting IG/high quality credit versus treasuries.

Low rated credit. This is a bet that the dollars allocated to distressed opportunities will have to chase the market. That so much money is being allocated to private credit, that they will compete more aggressively pushing spreads tighter. Finally, if the CLO arbitrage can be effective again (and it seems likely) the wave of new buyers of B- and CCC rated leveraged loans could be large, pushing those markets higher.

CDX should underperform bond spreads as it is more correlated with equities.

I like shorting bonds unhedged (through a vehicle like LQD). We can get cute and try and short credit spreads in the bond market, but for that, I prefer CDX as a tool, and think the all-in yield trade is a better idea right now.

Bottom Line

Maybe the party isn’t over, but I’ve had my fun and think it is time to run (okay, more of a quiet exit than anything too bearish, but I’m out of here!).

Tyler Durden

Thu, 12/21/2023 – 11:35