Fed Backs Self Into Corner Just As Inflation Revives

Authored by Simon White, Bloomberg macro strategist,

The magnitude of last week’s dovish swing by the Federal Reserve now makes a rate cut next year highly likely.

Yet, as is so often the case with central banks focused on lagging variables, it could come at exactly the wrong time, with a profusion of indicators showing inflation will be rekindled later next year. Rate-cut expectations look overdone, but any repricing may not come until the whites of inflation’s eyes are seen — when that happens the move will be dramatic.

No analogy is perfect.

But history rhymes because there is one thing that is immutable through time: human nature.

{kind=link}

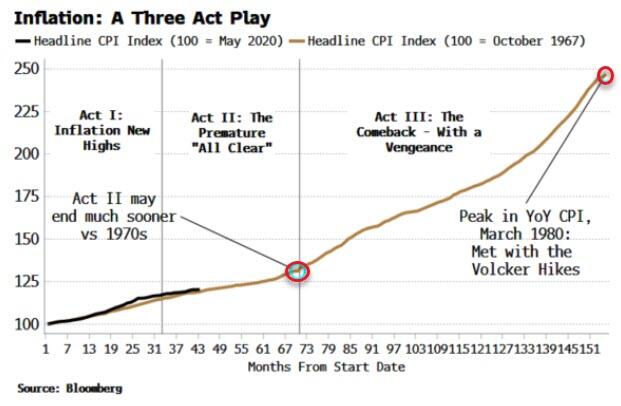

The 1970s were different to today in several respects, but the immutability of human behavior makes it quite conceivable a similar inflation pattern could recur.

In that decade, price growth was a Three Act Play: Act I was inflation making new highs after excessive easing from the Fed; Act II was the premature all clear, with rates getting cut when it was thought inflation was beaten; and Act III was the re-acceleration, when price growth unexpectedly began to climb again.

{kind=link}

People have a tendency to linearly extrapolate and thus miss turning points. The problem with inflation is that it is one of the most lagging of all economic variables — it typically troughs in the middle of expansions and peaks in recessions. We are likely heading toward a trough, with an increasing chorus of leading indicators showing inflation will start turning back up as early as the second half of next year.

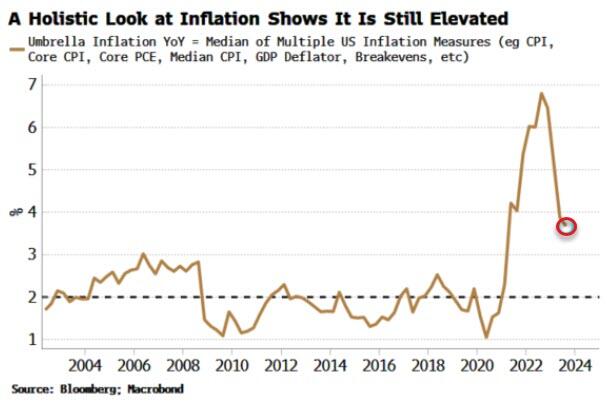

Focus is often on headline CPI, which has retraced 85% of the way from its recent highs toward the 2% target. But a more comprehensive look at inflation shows the drop has been much less dramatic, with the median of a broad set of price-growth measures still very elevated compared to pre-pandemic norms.

{kind=link}

Nonetheless, inflation’s steep decline is justifying the benign outlook the Fed and other central banks increasingly have. But a turning point looks very much on the cards. It’s starting to feel like we’re in the midst of Act II, the premature all-clear — and Act III is soon about to begin.

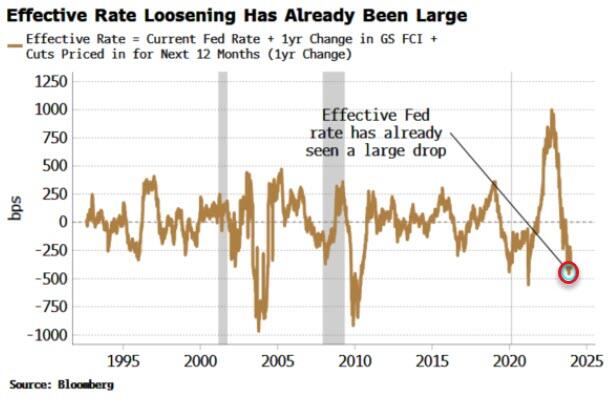

Note we have already had a large de facto easing in rates. Goldman Sachs’ Financial Conditions Index is designed such that it translates into an effective change in the Fed rate. If we add this implied fall in the policy rate due to the loosening in financial conditions to the cuts that are priced in by the market for next year, the effective Fed rate has already experienced a significant decline.

{kind=link}

Thus before the Fed has even cut rates, inflation potential has risen — and is why the Fed’s recent pivot is a monumental gamble.

We can see this pipeline inflation explicitly. The following charts need little commentary and show clearly from multiple angles that disinflation will soon be over, and price growth will begin rising again later next year.

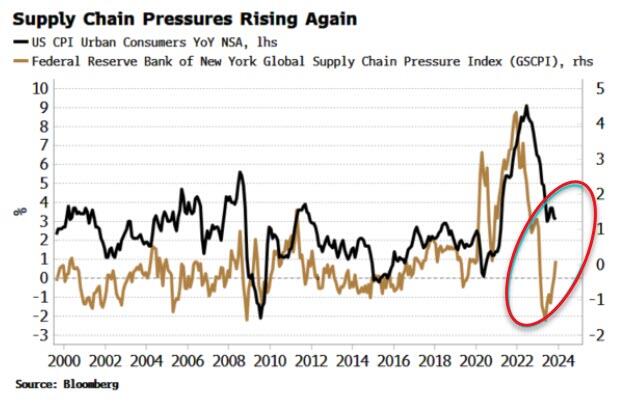

First is supply pressures. After easing significantly as the world came out of lockdown, they are now climbing quickly again. The fracas in the Red Sea is a reminder of how brittle supply chains are in a world of heightened geopolitical risks.

{kind=link}

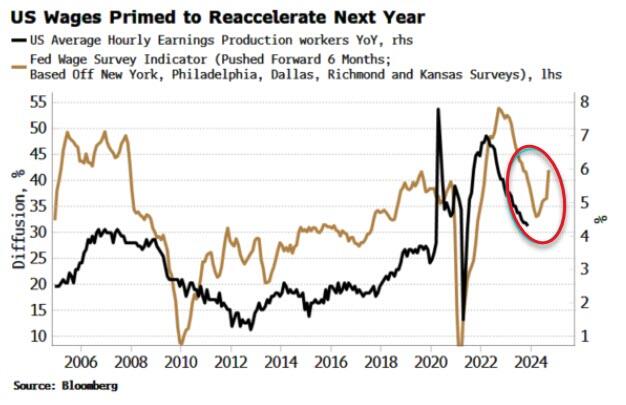

Next is wages. Wage growth has been falling, but remains positive in real terms. Importantly, leading indicators show wage growth will start to pick up again next year. The NFIB survey’s compensation plans component has started rising again, and the Fed regional wage surveys have picked up strongly, which lead average hourly earnings by about six months.

{kind=link}

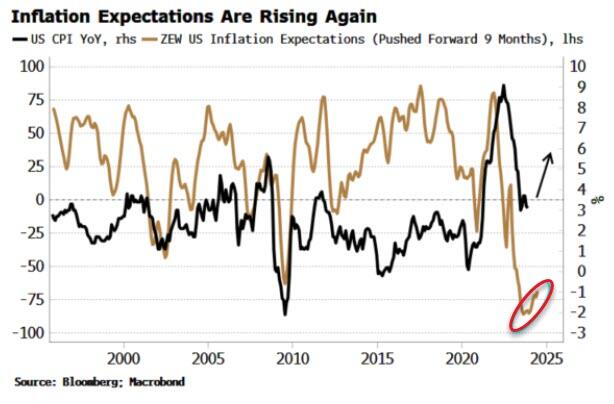

Third is inflation expectations. After seeing a steep fall when central banks were hiking, they have started to rise again.

{kind=link}

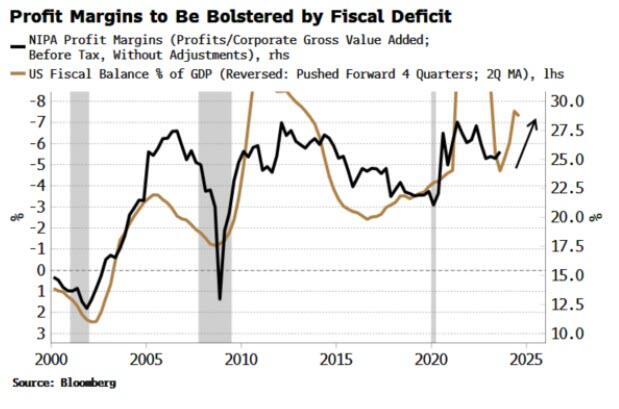

Then there is profits and profit margins. Profits are now the biggest contributor to corporate prices, in contrast to the decades before the pandemic, when labor costs were the largest driver. Profit margins fell after the pandemic, but they have stalled at a higher level. The large fiscal deficit is likely to push profit margins higher again next year.

{kind=link}

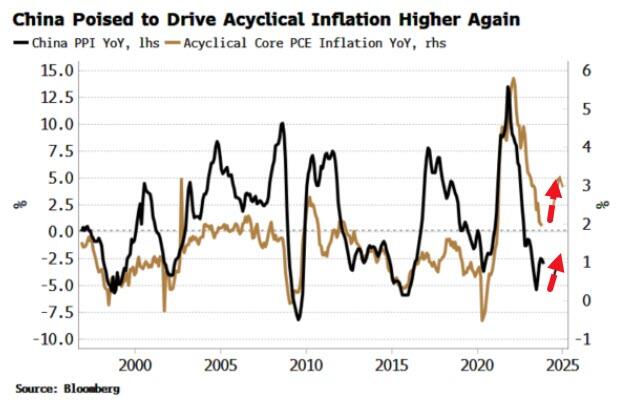

Fifth is China. It has been one of the key drivers of US and global disinflation (more so than the direct impact from central-bank rate hikes). The central government in China is using its capacity to borrow more to stimulate, while the PBOC is pumping increasingly more liquidity into the system. China is likely to turn a corner in 2024, which will stoke significant inflationary tailwinds.

{kind=link}

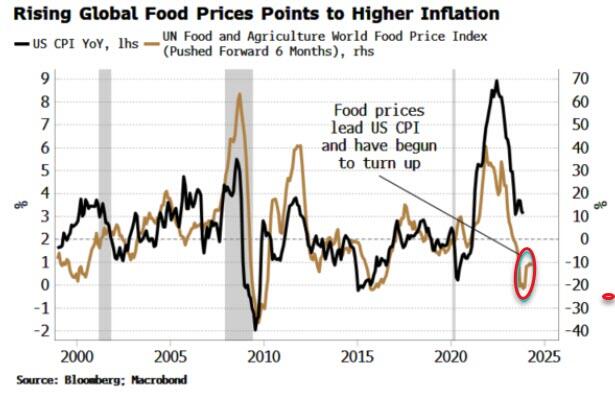

Then there are global good prices, which have started to rise again too. These lead US CPI by about six months.

{kind=link}

Finally, my leading indicator for inflation, which leads US CPI by six months, looks like it has stopped falling and is on the cusp of rising again.

{kind=link}

Most of US inflation’s fall has been driven by cyclical factors, e.g. energy. Structural inflation – defined as the sub-components of CPI that are persistently above their long-term average — has fallen too, but remains elevated (see chart below).

{kind=link}

Here lies the rub: structural inflation looks like it has started to turn back up while the risk of cyclical inflation turning up again too is rising (oil has been climbing), reinforcing the nascent rise in structural inflation.

The result: headline inflation begins to re-accelerate.

To miss one or two signs of rising inflation may be misfortune, but to miss at least eight looks like carelessness. With CPI fixing swaps seeing a continuation in the disinflationary trend through 2024, markets will likely have to re-adjust their inflation outlook at some point next year. However, the Fed’s fervent dovish conversion could see it cutting rates all the same — right when the third inflation act is about to begin.

Tyler Durden

Thu, 12/21/2023 – 13:20