Yen Plunges After BOJ’s Ueda Admits It’s “Difficult To Exit Negative Rates”, Shattering Normalization Hopes

Ahead of today’s BOJ decision, the latest “big” announcement by a major bank, expectations were hot and heavy that Japan, the country that introduced ZIRP, QE and NIRP to the world would magically abandon the only monetary policy that has prevented its bond market (of which the central bank owns over 100% of GDP) from collapsing into a fiscal singularity, and would if not hike rates after seven years of negative rates, then at least strongly guide to a January “normalization” liftoff. We, on the other hand, mocked market consensus, warning there was no way the BOJ would do this just as the Kishida government is on the verge of collapse, not to mention that real wages were at all time lows!

Kishida government on verge of collapse, approval rating at all time low, and real wages plunging at a record pace.

And market thinks they will somehow end NIRP.

— zerohedge (@zerohedge) December 18, 2023

Just a few hours later we were proven right again and consensus dead wrong, when not only did the BOJ not unveil anything transformational, or even new, of note,but much more shockingly, Governor Ueda admitted what we had been saying all along, namely that “it is difficult to lay out a plan for an exit from the negative rate.“

Specifically, in an announcement that came very early in the day indicating there was little to no discussion or debate on the topic of normalization, the Bank of Japan left their policy settings unchanged overnight, and didn’t offer any guidance on when they might move away from their negative interest rate policy.Additionally, following the meeting that was unexpectedly attended by a cabinet minister (to make sure there are no deviations from the dovish script), the BOJ said it would “patiently continue” with monetary easing and laid out forward guidance was not only not skewed to more tightening, but to even more easing.Translation: forget anything about normalization or a rate hike any time soon, and certainly not during the Kishida government.

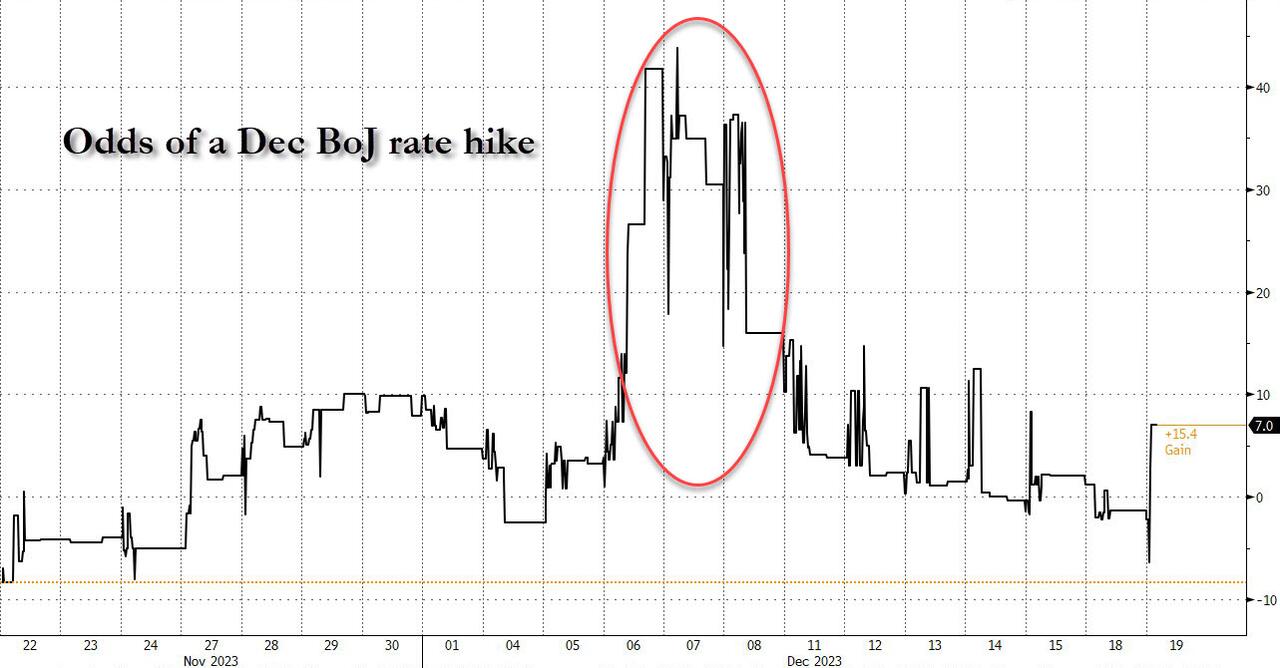

This was a problem because previously the BOJ had used both media leaks and direct jawboning, not to mention a series of explicit remarks hinting at liftoff, set expectations that the BOJ would signal a shift away from the policy over the months ahead (it was this meeting a year ago they made an unexpected adjustment to their yield curve control policy that took global markets by surprise). As a result, odds of a December rate hike hit a remarkable – and laughable – 40% at the start of the month, when the BOJ’s favorite mouthpiece, Nikkei Asia, published a report titled “BOJ lays groundwork for end of Japan’s negative rates“, which suckered in countless NPC lemmings into expecting a hawkish pivot by the BOJ, hilariously just as the Fed was about to flip dovish.

{kind=link}

And while the meeting itself was bad for Yen bulls, it was Ueda’s presser shortly after that crushed any hope of further yen appreciation. Determined to keep his options open, Ueda (who naturally didn’t rule out policy normalization at any of the coming meetings as that would destroy what little credibility the Bank of Jokers has left) insisted he first needs to see more evidence that the BOJ will achieve its price stability target, and added that policymakers are unlikely to give an explicit warning of an impending rate hike, largely discounting the kind of telegraphing sometimes employed by the Federal Reserve and the European Central Bank (spoiler alert: the reason why the BOJ will never give an “explicit warning” of a rate hike is because one will never take place).

“There isn’t much likelihood of us suddenly announcing that we’ll raise rates a month in advance,” Ueda said, having earlier remarked that surprises couldn’t always be avoided.

Some of his other comments are below:

Ueda said at this point it’s difficult to lay out a plan for an exit from the negative rate.He noted that there’s a lot of uncertainty about the outlook and can’t yet see if the inflation target will be achieved

Ueda said it’s too early to say price trends will meet the BOJ’s 2% inflation target. He needs to see more data to have enough confidence.

Ueda said he will pay attention to not just data but also to what he hears from market participants (the same market participants that get confused by every contradictory statement issued by Ueda, that is).

Ueda said he’s seen positive commentary on the outlook for wage hikes next year, and the chances of hitting the 2% inflation target are rising. And while he may be hopeful that next year’s spring wage hike negotiations yield some gains, the reality is that real wages in Japan are the lowest they have ever been (another reason why you can forget a rate hike every taking place).

{kind=link}

As a result his next comment was even more idiotic: “Bank of Japan Governor Kazuo Ueda says he’s hoping to see the impact of wage gains spread to consumer and services prices.” Well since real wages have never been lower, it’s kinda difficult to see “wage gains” spreading anywhere, isn’t it?

Puting it all together, the BOJ governor hilariously said that his remarks earlier this month about his job becoming ‘more challenging’ from year-end into next year were merely a general comment. In other words, all those who listened to what he said and traded accordingly, and were blown out in a flurry of stop losses, well, tough.

For speculators looking for more concrete hints of a January move, the decision and comments offered no support that view, especially since Ueda said it was too early to give specific details on any exit plans. This, coming at a time when Japan’s inflation is higher than the US, and set to tumble especially with the Fed now turning dovish, means that one can lose any expectations for normalization by the BOJ and instead just keep clipping that generous 5.5% carry that a long USDJPY position provides – which understandably shot up as much as 1.5% after the BOJ once again hammered yen longs…

{kind=link}

… while awaiting a burst in capital gains once the $20TN carry trade finally does blow up and sends the Japanese yen cratering into the failed currency abyss (as described here) which now is just a matter of time.

The yen had touched a four-month high last week after the Fed signaled its policy pivot coming in 2024. Those earlier gains took had taken some of the pressure off Ueda, who faced the risk of sending the currency to a fresh three-decade low at recent meetings.

There is another reason why one can kill any speculation for tightening by the BOJ: as Bloomberg notes, the Fed’s dovish turn isaputting a bookend on the timing for a BOJ policy move. If an end to the BOJ’s subzero rate were to trigger a much stronger yen, it would rekindle deflationary pressure in the economy. Pulling the plug on the negative rate when other central banks are starting to ease policy may also spark more volatility in markets.

While Ueda ruled out the Fed as a factor, saying the BOJ wouldn’t rush its policy decisions based on what it thinks the Fed might do in three or six months’ time, economists remained unconvinced.

“There is no doubt the Fed’s pivot is chilling the BOJ’s blood over its normalization plan,” Kumano said. “If the Fed cuts rates, for instance, after the BOJ’s April meeting, foreign exchange rates would end up getting a double punch that would prompt the yen to gain. That’s something the BOJ wants to avoid.”

Benchmark 10-year JGBs fell as much as 5.5 basis points from its intraday high to 0.63% as expectations of a looming rate hike collapsed. That compares with a peak of 0.97% for the yield in the wake of the late October BOJ meeting when Ueda added more flexibility to yield curve control.

Commenting on the BOJ’s decision, and putting it in the context of recent central bank decisions elsewhere, Bloomberg’s Ven Ram said that global rates are on hold through at least March of 2024. Here’s why:

For all the expectations of a tweak in policy guidance from the Bank of Japan, we barely got any.That suggests benchmark rates in the major global economies will be on hold in the first quarter — even though market pricing doesn’t acknowledge that fully.

The BOJ vowed to “patiently continue with monetary easing while nimbly responding to developments in economic activity and prices as well as financial conditions”. There was no sense of urgency that the central bank is about to exit its negative rate anytime soon.That said, it’s worth noting this guidance (italics mine):

“…As a virtuous cycle from income to spending gradually intensifies, Japan’s economy is projected to continue growing at a pace above its potential growth rate…Meanwhile, underlying CPI inflation is likely to increase gradually toward achieving the price stability target, as the output gap turns positive and as medium- to long-term inflation expectations and wage growth rise.”

That reference on underlying inflation and output gap was about the most hawkish bits from the statement. The focus on wage growth indicates that policymakers are likely to wait for shunto wage negotiations — which take place annually in the spring — to play out before deciding on their course of action. Which is why any move before April seems premature.

Over in the US, even the more dovish-leaning Federal Reserve officials — from Austan Goolsbee to Mary Daly — have all pushed back on the notion that we could get a rate cut as early as March. Even so, the markets aren’t quite buying it, with Fed fund futures ascribing a 75% chance for the first reduction by then.

European Central Bank officials have been at pains to emphasize that traders shouldn’t be factoring in a rate cut by March. And pricing surrounding that meeting has responded much more to that guidance (32% now versus 64% after the ECB’s meeting last week) than in the US.

Meanwhile, Bank of Canada Governor Tiff Macklem said overnight that he wants to see “not one or two months”, but “a number of months” of slowing inflation before we could get a rate cut. Even so, traders are more than fully pricing a reduction by April there.

From all indications, it looks like key interest rates around the major economies will stay put through the first quarter— but in some corners traders haven’t quite embraced that message yet.

Tyler Durden

Tue, 12/19/2023 – 10:20