Red Sea Blockage Means A New Round Of Surging Cost-Push Inflation

By Maartje Wijffelaars, Senior Economist at Rabobank

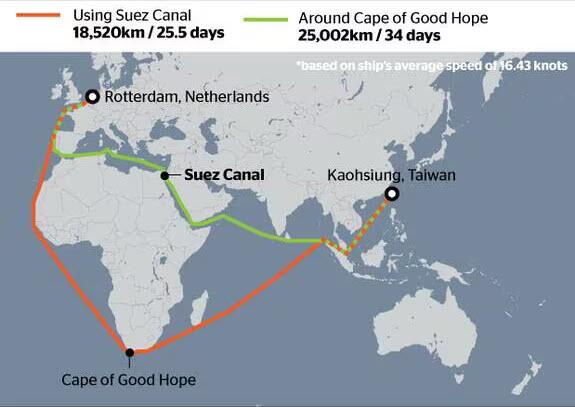

Rerouting

Yesterday, BP and Norway’s Equinor ASA joined the slew of vessel owners that have paused transit through the Red Sea, and hence the Suez Canal. Some have already taken a detour around the Cape of Good Hope, lengthening travel time by some 8 to 15 days, while others are waiting for further instructions and/or military protection. By Sunday, 55 ships had yet rerouted since Houthi’s haijacked the Galaxy Leader at 19 November, while 2128 vessels had passed through the Suez Canal, according to the managing director of the Suez Canal Authority. Some 78 are said to be awaiting instructions. Given that 12% of global trade runs through the canal, a back of the envelope calculation suggests that disruptions to date concern less than 1% of global trade.

{kind=link}

Still, the longer it takes and the more companies start avoiding the transit, the greater the disruptions. Given the possible magnitude, on a global scale countries are talking to join forces to protect vessels sailing the red see and to find a way to stop the Houthi attacks. The US has already sent warships to intercept attacks and a coalition of countries has now agreed to jointly carry out patrols.Yet it is unclear to what extent they will actually be able to guarantee a safe transit. If anything the risk of a new round of cost-push induced inflation has increased substantially. Inflation surprises back in 2021-22 have been associated with supply-chain disruptions, with the IMF arguing that those shocks added around 1% to global core inflation. We, at the time, estimated the cumulative impact of inflation surprises at around 3%-points for the Eurozone. Although the current situation isn’t directly comparable, the recent past does underscore that this could potentially affect inflation.

Indeed, while rerouting implies shipping companies save high Suez transit fees, rerouting comes with significant costs for container ships due to the lengthening of the journey and higher fuel needs.Meanwhile, insurance costs for travel over the Red Sea have increased almost tenfold since the Houthi attacks began, according to Bloomberg. Finally, given that rerouting would increase the number of days a commercial vessel or fuel tanker is unavailable, it lowers global available capacity, which should also put upward pressure on freight prices – at a time when drought at the Panama Canal has already pushed up prices for especially bulk transport.

That said, oversupply in the container market following the large increase in the number of ships in the aftermath of the pandemic combined with weak demand acts as a softener, for now. The composite container freight benchmark rate has come of its recent low and increased by over 10% over the past weeks. But it is still cheaper than during most of the year and 6 to 7 times as cheap as during the pandemic.

Turning to energy, recent developments have not yet impacted crude supply, but has pushed prices a bit given the risks highlighted above. 4.5% of global crude oil, 9% of refined products, and 8% of liquefied natural gas (LNG) tankers transit through the Suez Canal. Brent oil futures increased yesterday by 1.8% to USD 78,12 per barrel. This is also clearly higher than its recent low of around USD 73 a week ago, but still substantially below its post-conflict peak of USD 92 mid-October. Meanwhile, the TTF gas price one-month ahead, rose yesterday after weeks of decline, but has come down again already in this morning’s session. Weak demand combined with ample supply is keeping a lid on prices, it outweighs the impact of risks of severe supply disruptions, for now.That said, volatility is back up and there is some upside risk to prices as the first LNG tankers are now rerouting around the Cape.

It is clear that supply chain disruptions add upward risks to the inflation outlook.

In other news, yesterday European Council President Charles Michel announced that EU leaders will convene on an emergency summit on 1 February to agree over the bloc’s budget and financial support for Ukraine. Last week, the EU postponed the vote on a four-year EUR 50bn aid package for Ukraine until January due to Hungarian objections. The package was supposed to be agreed during an EU summit on December 14-15, showing that the release of previously frozen EU support fund worth EUR10bn to Hungary have not been sufficient to persuade Hungary to lift its veto. The pay-out of another EUR 30bn is being upheld since last year – due to backsliding on judicial and anti-corruption reforms -, and Orban has stated it would not support more funds flowing to Ukraine until all frozen funds have been transferred. The major question is whether the EU will give in. Withholding support to Ukraine would play into the hands of Russia, especially now US support also hinges in the balance and at least is being delayed. Yet giving in to Orbán’s alleged blackmail would clearly display EU governance weaknesses. A suggested work around could be that all EU countries bundle funds outside the EU budget, as such a mechanism would not require the approval of Hungary.

Finally, as expected, the BOJ has not hiked its negative overnight policy rate, as it waits for more confirmation that wage growth is indeed set to solidly push inflation higher. Governor Kazuo Ueda acknowledges that the the probability of a virtuous cycle between wages and inflation is “gradually increasing”. Yet he wants more confirmation that higher wages indeed spread to prices, before lifting the world’s last negative policy rate. Indeed, even though negotiated wages increased most in 30 years this year, there is no guarantee just yet that higher wage rises will also be paid to the majority of ununionized Japanese workers, argues our FX Strategist Jane Foley in a note published yesterday.

If anything, it is very clear that the BoJ deems it more costly to pre-emptively exit from accommodative policy than to act late.Still, given that the odds are currently favouring further policy normalisation next year, while other G10 central banks are likely to cut rates, we expect the JPY to have a better year in 2024. We have revised down our 12-month USD/JPY forecast to 135 from 140.

Tyler Durden

Tue, 12/19/2023 – 12:00