Fed’s Monumental Gamble Ensures Inflation’s Return

Authored by Simon White, Bloomberg macro strategist,

Follow the money. That’s how to explain the Federal Reserve’s extraordinary dovish swing last week. The government’s soaring interest-rate bill will become an increasing drain on the volume and velocity of reserves in the system, stoking headwinds for assets and the economy. By jettisoning higher for longer, the Fed has enabled interest-rate costs to fall – but only by heightening future inflation risks and the prospect of higher yields.

Mark Wednesday 13th of December down as the day modern-era central-banking independence died in all but name.The rot began several years ago, and spread when inflation jumped to its highest level in decades. But the Fed’s Damascene conversion to dovishness at last week’s meeting was the fatal blow.

There’s been plenty of speculation that politics drove the decision, especially with an election next year. But politics is heavily influenced by the expected state of the economy and the health of the markets, both of which ultimately come down to liquidity. It’s unnecessary to speculate on how politically driven the Fed is – its motives can be explained by following the money.

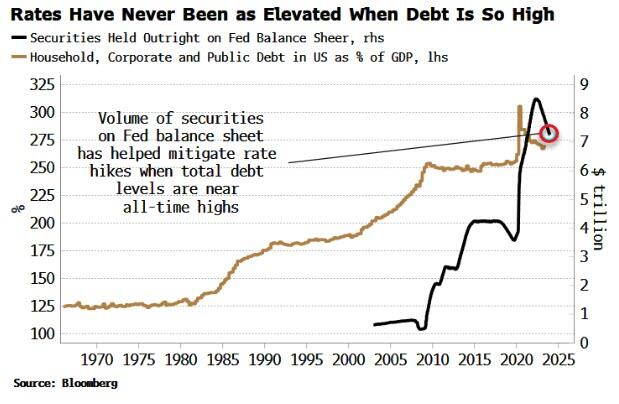

The central bank has been walking a tightrope as it has had to significantly raise rates when total debt and the size of its balance sheet have never been greater. How to tighten policy, dampen price growth, yet not trigger a financial crisis?

{kind=link}

First, the Fed has only allowed its balance sheet to shrink slowly.

Limiting the decline to at most $95 billion per month has meant that even after almost 18 months of quantitative tightening the central bank is still warehousing over $7 trillion of duration risk.

Second, and more importantly, the Treasury has decided to run its largest peacetime, non-recessionary fiscal deficit.

This was not the Fed’s choice, of course, but it presents a problem: such a large deficit when policy is already tight would threaten market stability as Treasuries de facto crowd out other assets.

But this was when Yellen enacted the “Treasury pivot”, a year before Powell’s last week.The Treasury, by pivoting issuance toward bills, meant money-market funds were able to fund the majority of the government’s borrowing needs using idle liquidity parked on the Fed’s balance sheet in the reverse repo (RRP) facility.

{kind=link}

Voila! We had almost $2 trillion of economically-supportive government spending and rising reserves – despite ongoing QT – fueling the “everything rally”.

This was a “cake-and-eat-it” fiscal deficit on speed.

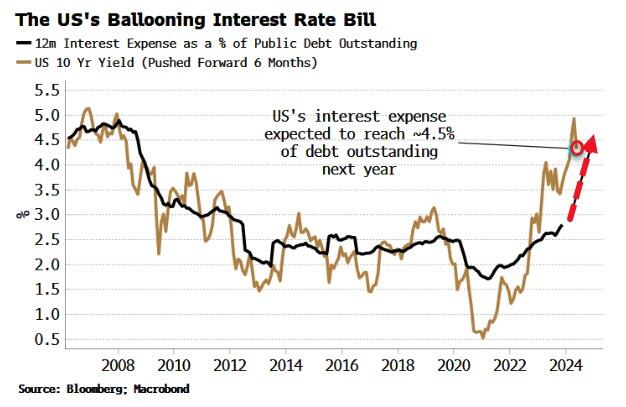

But all this issuance meant the government’s interest-rate bill started to rocket.

Moreover, rising Treasury yields pointed to the annual interest expense charging even higher next year, reaching in the region of $1.5 trillion, or about the GDP of Spain.

{kind=link}

Here’s the punchline: if this was allowed to continue unchecked it would turn a benign environment for reserves into one very unfavorable for markets and the economy.

Liquidity would tighten rapidly, posing a formidable headwind for assets, as well as threatening funding markets and financial stability.

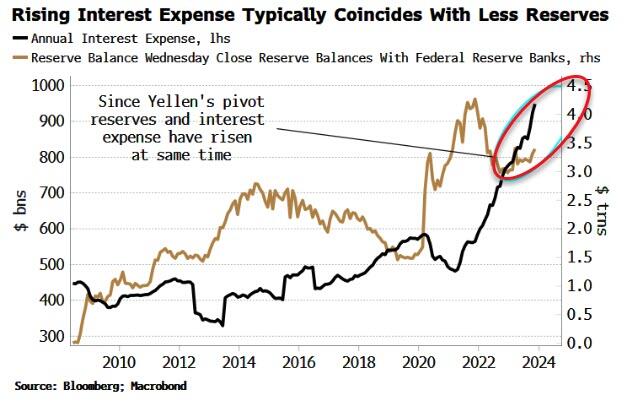

Viewed this way, Powell had to act.The chart below shows why: rising government interest costs typically coincide with falling reserves, i.e. they lower liquidity.

{kind=link}

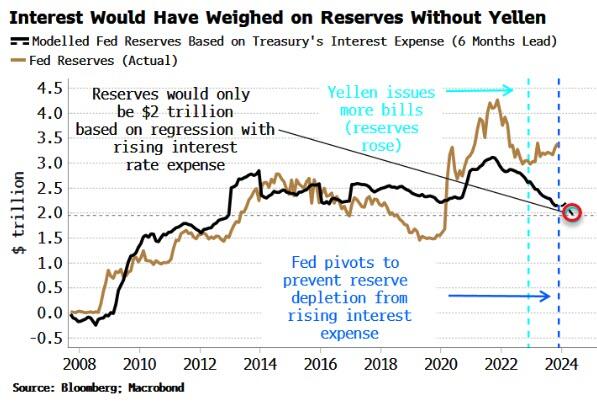

Since the Yellen pivot, however, reserves and the interest expense have risen at the same time. But that can’t continue indefinitely. The black line in the chart below shows reserves next year would be under $2 trillion – considered below what is sufficient for the smooth running of the financial system – based on a simple regression with the rising interest cost.

{kind=link}

Yellen’s pivot arrested the fall in reserves this year, and meant they rose when they would likely already be falling due to QT. But the ballooning interest-rate bill would soon prove too much and drag reserves lower. Cue Powell’s pivot last week.

The sheer growth in interest costs has been quite spectacular.As shown above, the 10-year yield is a very good proxy for the government’s interest-rate bill. The alarm likely grew in the Treasury and the Fed as the yield curve started to bear-steepen and term premium began to rise, pointing to the bill getting ever larger.

That’s not a problem, some argue, since the government paying interest is stimulatory as the money will come back into the economy. But it’s highly doubtful much of it would.

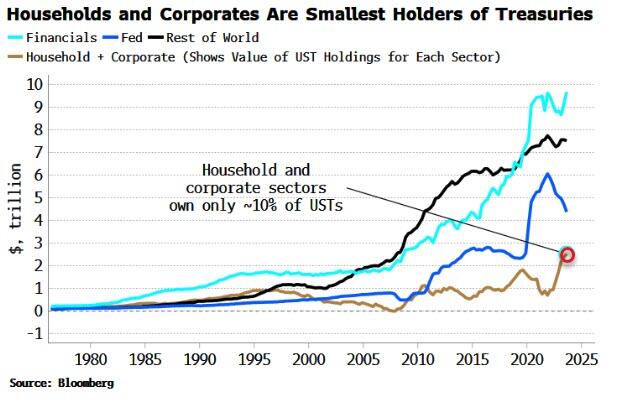

Only the household and corporate sectors are likely to spend interest income remitted to them (and then only some of it). But they are the smallest holders of Treasuries, owning only ~10% of the outstanding. Even adding in what they own via stock holdings (e.g. bond ETFs), those sectors are minority holders of Treasuries. They are dwarfed by financials and foreigners – who are more likely to either reinvest it, or spend it abroad. Neither is inclined to spend much of it in the economy.

{kind=link}

Reserve velocity will fall as the government will pay its rising interest rate bill through taxes and more borrowing. Taxes are paid with bank deposits, the proceeds of which – as explained above – go to entities which are more likely to reinvest the proceeds rather than spend them. The reserves are still in the system (only the Fed can eliminate them) but they are now held by savers with a lower propensity to spend – i.e. reserve velocity has declined.

A rise in borrowing leads to a similar outcome, especially as the RRP depletes and is no longer able to act as a liquidity buffer to the government’s borrowing and ongoing QT.

Reserves could even see an outright fall from rising interest costs, amplifying QT, if they were invested in money market funds, which in turn put the proceeds in the RRP if its rate becomes more attractive versus bills (either due to the Fed’s pivot lowering front-end rates, or the Treasury issuing fewer bills).

This year’s favorable set of circumstances that has supported the market and the economy are thus destined to become more hostile as the government’s interest-rate bill spirals. Yellen’s pivot kept the game going this year; Powell’s pivot is to buy more time next year.

It’s a monumental gamble, though. Inflation is showing signs of stickiness and some leading indicators are pointing to a re-rise in price growth.

The seeds of the next Fed pivot have just been sown in the last.

Tyler Durden

Tue, 12/19/2023 – 09:35