Risk-Asset Tailwinds Grow As Global Liquidity Ends Year On High

Authored by Simon White, Bloomberg macro strategist,

Global liquidity is ending the year on a very strong footing, supporting risk assets.

Liquidity conditions for most of this year have generally been favorable, but they have received a boost in recent weeks from the Federal Reserve and the PBOC, ensuring that the end of this year and the start of 2024 will be even more liquidity friendly.

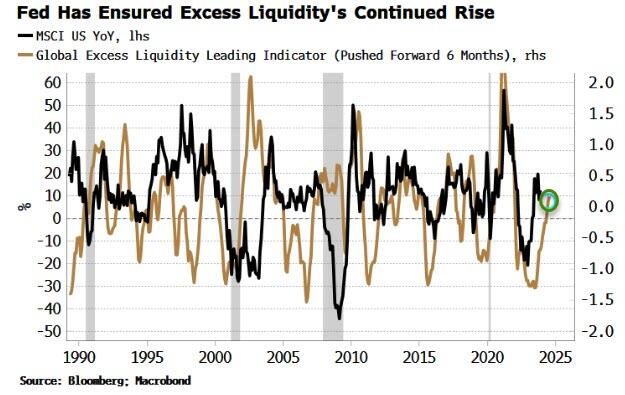

Global excess liquidity – the difference between real M1 growth and economic growth for the G10 in USD terms – was on the cusp of rolling over. However, the Fed’s abrupt dovish pivot last week will lift excess liquidity through a weaker dollar, as well as supporting global money growth by the green light it gave to an end to “higher for longer” for the major DM central banks.

{kind=link}

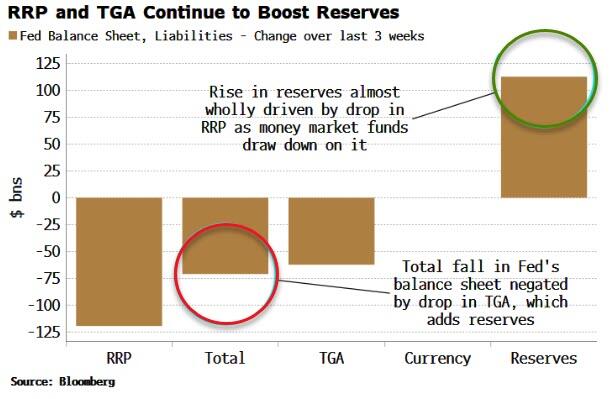

Moreover, in the US, reserves continue to rise. Despite quantitative tightening, reserves are higher than they were when QT started last year, with that rise accelerating in recent weeks. Reserves have increased over $100 billion in the last three weeks, driven almost wholly by a decline in the reverse repo (RRP) facility, as money market funds draw down on it to buy t-bills.

{kind=link}

The fall in the Treasury’s account at the Fed of around $60 billion in the last three weeks has negated what would have been a ~$70 billion decline in reserves from QT.

In China, liquidity is being added at an increasing rate. Net injections of liquidity by the PBOC from repo and the medium-term lending facility have risen sharply in recent months, and sit at just under CNY 4 trillion on a 12-month sum basis.

{kind=link}

China’s data has been dismal. Inflation is negative and money growth has been weak, but the net injections of liquidity demonstrate policymakers are amping up the support for the economy.

Unusually, China has been a drag on global money growth over the last few years; unlike most of the last decade and a half where it has been a major driver of it. A re-acceleration in China’s money growth would radically upset the benign inflation environment foreseen by the Fed et al.

Either way, the global liquidity backdrop is strong at the moment, which will act as a solid tailwind for stocksand other risk assets into the end of this year and the next.

Tyler Durden

Mon, 12/18/2023 – 08:40