Key Events This Pre-Holiday Week: BOJ, PCE, Durables And A Some Other B-List Things

With all major macro events for 2023 now in the rearview mirror as trading desks empty out and just junior traders staff Wall Street’s skeleton crews, the week ahead will be a much quieter one as we move towards Christmas. But central banks will still be in focus as the Bank of Japan announce their latest decision tomorrow. And, as DB’s Henry Allen notes, unlike other central banks where the focus is now on rate cuts, the speculation around the BoJ is still around when the negative interest rate policy might come to an end (TL/DR: never,especially with the current government in peril of collapse and the last thing it wants is to hike rates). Indeed, there had been heightened speculation over the last couple of weeks about a policy shift at this meeting, and as recently as December 7, investors were pricing in a 45% chance intraday that there would be a shift away from the negative interest rate policy. However, that’s fallen back significantly, and Bloomberg also reported last week that BoJ officials saw little need to change policy this week. DB’s economist thinks that they’ll maintain their current monetary policy framework this time, but that they’ll also hint in some way at an end to the negative interest rate policy in January. See the full preview here.

When it comes to economic data, inflation readings will still be in focus, particularly in terms of what that means for how swiftly central banks can cut rates. This week brings several releases, including the November CPI prints from the UK, Canada and Japan, along with the PCE inflation release from the US, which is the Fed’s preferred measure of inflation.In October, US headline PCE was down to just 3.0% year-on-year, which is the lowest rate since March 2021, adding further support to hopes of a soft landing and near-term rate cuts.

{kind=link}

Finally, we’ve also got several confidence indicators, including the Ifo business climate indicator from Germany, the Conference Board’s consumer confidence in the US, along with the European Commission’s consumer confidence reading for the Euro Area.

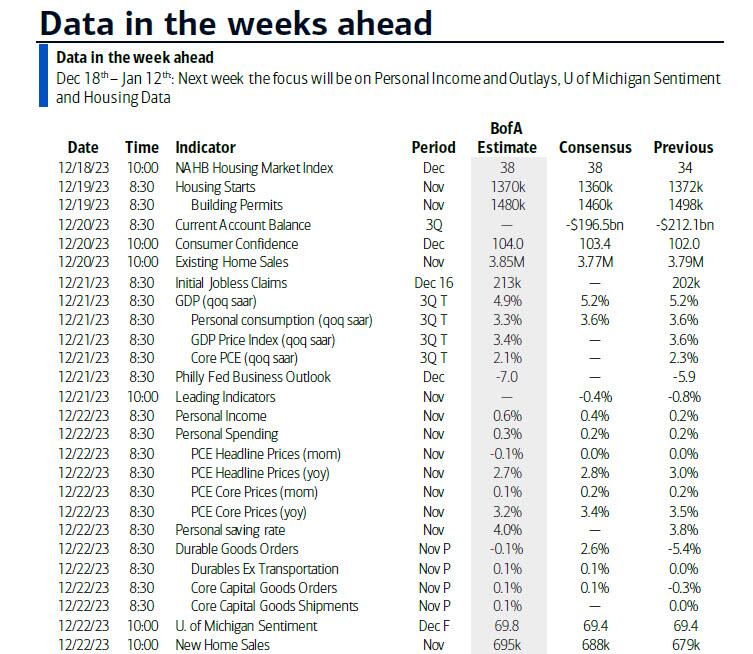

Courtesy of Rabobank and DB, here is a day-by-day calendar of events

Monday, December 18

Data:A slow day for data. Q4 consumer confidence for New Zealand at 88.9 was a much stronger print than the prior reading of 80.2. The Performance Services Index also recorded a rise from 49.2 in the prior month to 51.2 in November. In the European session we will see Q3 labour costs data for Spain and the German IFO survey for December. ‘Current Assessment’ is seen largely unchanged, but the Bloomberg survey suggests minor improvements to the ‘Business Climate’ and ‘Expectations’ readings.

Central banks:ECB’s conference on fiscal policy and EMU governance (through December 19), Schnabel, Vujcic, Wunsch and Lane speak, BoE’s Broadbent speaks

Tuesday, December 19:

Data:The highlight of the day will be the BOJ policy meeting. The policy rate is expected to remain unchanged at -0.1% and the 10-year JGB yield target at 0%. Don’t be surprised if there are some hawkish signals from the BOJ though, it was only a week or two ago that the market was getting excited at suggestions that this meeting could see liftoff for the policy rate. New Zealand trade balance figures for November also land on Tuesday. Will recent upgrades to dairy prices see a pickup in exports? We also get business confidence figures for NZ and then the release of the minutes of the RBA’s December policy meeting (the one where they did nothing). Later in the day we will see US housing starts and Canadian CPI for November, where prices are expected to fall by 0.2% m-o-m (+2.8% y-o-y).

Central banks:BoJ decision, Fed’s Bostic speaks, ECB’s Simkus, Kazimir and Vujcic speak, BoE’s Breeden spreaks

Earnings:Accenture, FedEx

Wednesday, December 20:

Data:The key data releases of the day will be the PBOC’s decision on the 1-year and 5-year loan prime rates. No changes expected to either, but it’s worth keeping an eye on this release after the PBOC injected $112bn of new liquidity into the market last week via it’s 1-year MLF facility. UK CPI figures for November is the other big release of the day. CPI is expected to drop to 4.4% from 4.6% in October. Wednesday morning brings consumer confidence figures for NZ and the Westpac leading index for Australia. Following that we will see November trade data for Japan, as well as German producer price inflation, German GfK consumer confidence and UK PPI. Over in the United States we will see MBA mortgage applications, existing home sales and the Conference Board’s consumer confidence survey. The Bank of Canada will also be releasing its latest Summary of Deliberations.

Central banks:BoC’s summary of deliberations, ECB’s Lane speaks, China 1-y and

5-y loan prime rates

Earnings:Micron, General Mills

Auctions:US 20-y Bond ($13bn, reopening)

Thursday, December 21:

Data:Thursday will be dominated by a slew of second-tier data until we see October retail sales for Canada (0.8% m-o-m expected), the third read of Q3 GDP in the USA, the usual weekly jobless claims data, the Philly Fed’s Business Outlook and the Conference Board’s leading index. Earlier in the day we get business and manufacturing confidence figures for France, French retail sales for November, Italian PPI for November and the December Lloyd’s business barometer for the UK.

Central banks:BoJ’s minutes of October meeting, ECB’s Lane speaks

Earnings:Nike

Auctions:US 5-y TIPS ($20bn, reopening)

Friday, December 22:

Data: US November personal income and spending, PCE deflator, new home sales, durable goods orders, December Kansas City Fed services activity, UK Q3 current account balance, November retail sales, Germany November import price index, Italy October industrial sales, December manufacturing confidence, economic sentiment, consumer confidence index, France November PPI, December consumer confidence, Canada October GDP

Finally, looking at just the US, Goldman notes that the key economic data releases this week are the Philly Fed index on Thursday and the durable goods report and core PCE inflation data on Friday.Chicago Fed President Goolsbee and Atlanta Fed President Bostic are scheduled to speak.

Monday, December 18

08:30 AM Chicago Fed President Goolsbee (FOMC voter) speaks;Chicago Fed President Austan Goolsbee will participate in an interview with CNBC. On December 15, Goolsbee said, “It’s clear we’re moving more toward a balanced environment, and as we do that, and as inflation comes down, we’ve got to think about how restrictive do we want to be and are there dangers on the employment side of the mandate? Just like we’ve…had these dangers on the inflation side of the mandate…We should be prepared to raise rates if we stop getting good news and it looks like we’re not on path to get down to [the Fed’s target] but also if we see inflation going down more than we expected, we should be prepared to recognize whether that level of restrictiveness that we’re at now, which is clearly restrictive, whether that’s appropriate and whether we should loosen [the policy rate].”

10:00 AM NAHB housing market index, December (consensus 37, last 34)

Tuesday, December 19

08:30 AM Housing starts, November (GS -0.5%, consensus -0.9%, last +1.9%);Building permits, November (consensus -2.5%, last +1.8%)

12:30 PM Atlanta Fed President Bostic (FOMC non-voter) speaks:Atlanta Fed President Raphael Bostic will speak on the US economy, the outlook for business, and the Fed’s role at a fireside chat. Q&A with audience is expected. On December 15, Bostic said he expects cuts “sometime in the third quarter” of 2024, with two cuts next year. He said, “I’m not really feeling that this [cutting] is an imminent thing” and that policymakers still need “several months” to accumulate data and confidence that inflation will continue falling. “I am going to try not to presuppose anything at this point…We’ve been surprised throughout the pandemic on a number of fronts, some to the good and some to the bad. And so I just don’t want to get anchored too much.”

06:00 PM Chicago Fed President Goolsbee (FOMC voter) speaks:Chicago Fed President Austan Goolsbee will participate in an interview with Fox News. The exact time is TBD.

Wednesday, December 20

08:30 AM Current account balance, Q3 (consensus -$196.0bn, last -$212.1bn)

10:00 AM Existing home sales, November (GS -2.5%, consensus -0.5%, last -4.1%)

10:00 AM Conference Board consumer confidence, December (GS 103.9, consensus 104.0, last 102.0)

12:00 PM Chicago Fed President Goolsbee (FOMC voter) speaks:Chicago Fed President Austan Goolsbee will speak on the WSJ’s Take on the Week podcast. Excerpts from the interview were published on December 15th. The exact release time is TBD.

Thursday, December 21

08:30 AM Initial jobless claims, week ended December 16 (GS 215k, consensus 215k, last 201k);Continuing jobless claims, week ended December 9 (GS 1,895k, consensus 1,675k, last 1,662k)

08:30 AM GDP (third), Q3 (GS +5.2%, consensus +5.2%, last +5.2%); Personal consumption, Q3 (GS +3.6%, consensus +3.6%, last +3.6%):We assume no revision on net in the third vintage of the Q3 GDP report (previously reported at +5.2% qoq ar).

08:30 AM Philadelphia Fed manufacturing index, December (GS -5.9, consensus -3.0, last -5.9);We estimate that the Philadelphia Fed manufacturing index was unchanged at -5.9pt in December, reflecting the rebound in East Asian industrial activity but downward convergence toward other manufacturing surveys.

11:00 AM Kansas City Fed manufacturing index, June (last -2)

Friday, December 22

08:30 AM Personal spending, November (GS +0.2%, consensus +0.2%, last +0.2%); Personal income, November (GS +0.5%, consensus +0.4%, last +0.4%) ;PCE price index, November (GS flat, consensus flat, last flat); Core PCE price index, November (GS +0.07%, consensus +0.2%, last +0.2%):We estimate personal spending increased 0.2% and personal income increased 0.5% in November. We estimate that the core PCE price index rose 0.07% in November, corresponding to a year-over-year rate of +3.11%. Additionally, we expect that the headline PCE price index was unchanged in November and increased 2.67% from a year earlier. Our forecast is consistent with core services ex housing inflation of 0.11% (mom sa) and with a 0.17% increase in our trimmed core PCE measure (vs. 0.17% in October and 0.29% in September).

08:30 AM Durable goods orders, November preliminary (GS +3.5%, consensus +2.2%, last -5.4%); Durable goods orders ex-transportation, November preliminary (GS +0.3%, consensus +0.1%, last flat); Core capital goods orders, November preliminary (GS -0.3%, consensus +0.1%, last -0.3%); Core capital goods shipments, November preliminary (GS +0.3%, consensus +0.1%, last flat):We estimate that durable goods orders rose 3.5% in the preliminary November report (mom sa), reflecting a jump in commercial aircraft orders. We forecast firm details as well, including a 0.3% rise in both core capital goods orders and core capital goods shipments. Our forecast reflects the rebound in East Asian manufacturing activity and the rise in industrial production of business equipment in November.

10:00 AM New home sales, November (GS +1.6%, consensus +1.5%, last -5.6%)

10:00 AM University of Michigan consumer sentiment, December final (GS 70.0, consensus 69.4, last 69.4); University of Michigan 5–10-year inflation expectations, December final (GS 2.8%, consensus 2.8%, last 2.8%):We expect the University of Michigan consumer sentiment index to rise 0.6pt to 70.0 and for the report’s measure of long-term inflation expectations to be unrevised at 2.8%.

Source: DB, GS, Rabobank

Tyler Durden

Mon, 12/18/2023 – 10:30