Santa Powell Unleashes Global “Buy Everything” Frenzy As Dollar, Yields Tumble

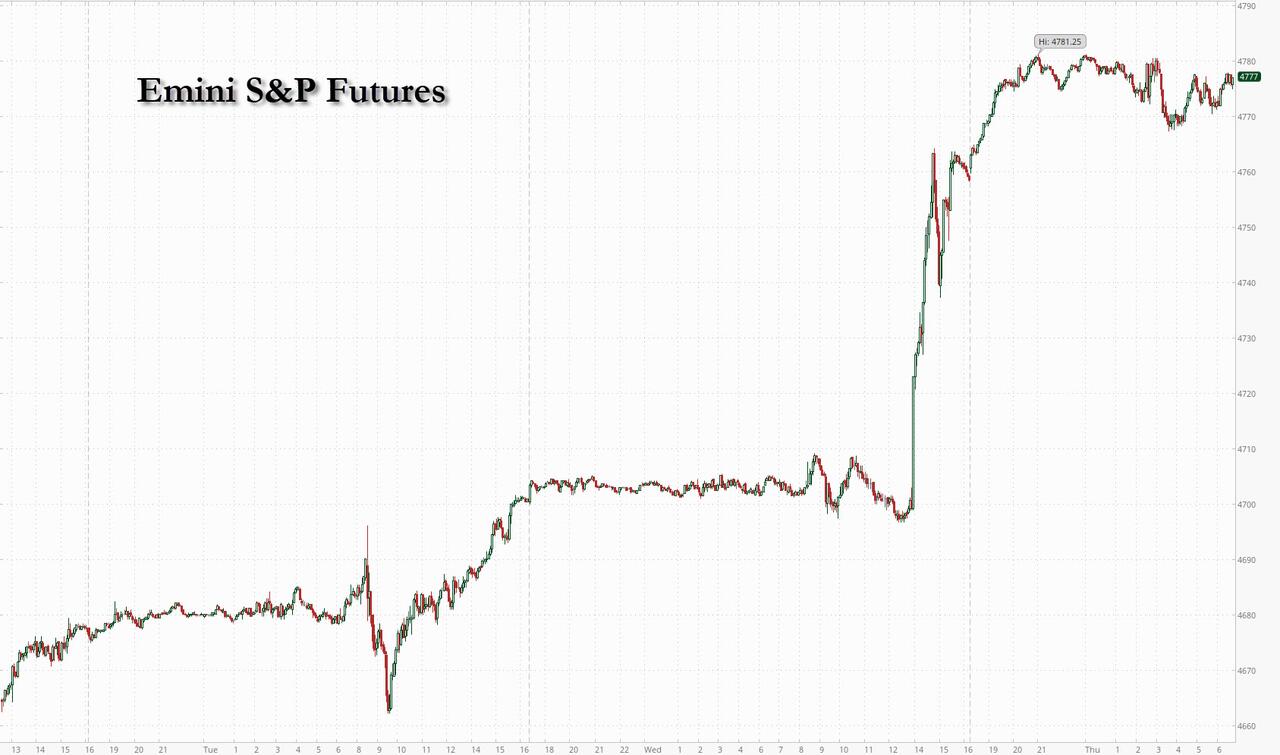

Virtually every risk asset across the globe is rallying this morning, as the dollar and interest rates get whacked after the Fed unexpectedly signaled a much more dovish outlook including more than expected interest-rate cuts next year, unleashing bullish euphoria across markets amid optimism that inflation pressures are easing. After the Dow already tipped into record territory yesterday, on Thursday it was tech’s turn – Nasdaq 100 futures climbed, setting up the index for a run at a record close; meanwhile S&P 500 contracts edged 0.3% higher after the benchmark ended within 2% of its record high on Wednesday. Europe’s Stoxx 600 index surged as much as 1.7%. Shares in Germany and France hit fresh all-time peaks. Bond yields are lower with the bulk of the curve seeing a bull steepening and the 10Y now well below 4% (3.94% last). The USD sell-off continues which in turn is helping to boost commodities where Energy is leading and $70 is now acting as support for WTI. The macro data focus is on Retail Sales and Jobless Claims: given the upside surprise delivered by the Fed, this data may not be market-moving but remain useful for understanding whether the growth without inflation hypothesis remains intact.

{kind=link}

In premarket trading, Adobe shares are down 6.1% after the software company gave a full-year forecast that is weaker than expected on key metrics. Separately, it also disclosed that the US FTC has been investigating the company’s subscription cancellation practices for more than a year. Here are some other notable premarket movers:

AerSale shares fall 11% after the company announced a secondary offering of 4 million shares.

AngloGold Ashanti shares rise 6.0% in New York as South African precious-metals shares rally. Gold gained after the Federal Reserve gave the clearest signal yet that its aggressive interest-rate tightening campaign has ended. Pro

Pagaya Technologies shares rise 6.5% as Jefferies initiates coverage on the fintech company’s stock with a recommendation of buy. The broker notes that the firm’s business model creates “a powerful network effect.

According to JPM strategists, the market narrative has shifted forcefully to soft landing which may be supported by upcoming Fedspeak and reflected in the yield curve, with JPM saying that we now “wait and see if the SPX can breach 4,800 before year-end.” The risk-on rush follows a pivot to looser policy by the Fed, which held rates steady Wednesday and forecast that their next moves would be lower. Policymakers’ projections in the “dot plot” showed 75 basis points of reductions in 2024, but traders are even more optimistic, betting on cuts of twice that magnitude.

“There’s been a lot of debate in recent weeks about whether investors are getting ahead of themselves, too optimistic about how quickly the Fed will cut rates — but the message from the central bank is that is not the case,”said Craig Erlam, senior market analyst at Oanda.

Indeed, some strategists are wary that much of the latest upswing in equities has been powered by the more speculative corners of the market — ranging from unprofitable tech stocks, to regional US banks and battered Swedish real estate. There are warnings that the exuberance might have gone too far. “We’ve seen something of an everything rally and for some parts of the market, the fundamentals don’t really support that,”said Kiran Ganesh, a multi-asset strategist at UBS Global Wealth Management.

Valuations and technicals also suggest stocks are vulnerable to a pullback in the short-term. The S&P 500 and Nasdaq 100 indexes have seen their relative strength indicator — a 0-100 gauge of bullish and bearish price momentum — soar into overbought territory, typically seen as a signal that a decline is imminent.And equties could remain at risk in the event of a downturn, said Joost van Leenders, senior investment strategist at Van Lanschot Kempen. “Whether rate cuts are positive for equities depends on the economy,” he said. “In a soft landing a pivot would be positive. But when the economy slips into recession, rate cuts traditionally don’t prevent a selloff in equities.”

* * *

In contrast with the Fed, the Bank of England said Thursday that “there is still some way to go” in the fight to control inflation, keeping interest rates at the highest level in 15 years. The pound strengthened and UK government bonds pared their gains after the decision. A rates decision from the European Central Bank is up next on a busy day for policymakers in the region.

Data readings on US retail sales and initial jobless claims due later Thursday will provide an early test of the buoyant mood among investors. Traders would be concerned by any surprises in the data that cloud the view that the surge in inflation has been contained without a significant cost to employment.

In Europe, the Stoxx 600 erupted another 1.6%, pushing stocks to fresh 2023 highs. European real estate stocks soared while Swedish property shares also got a boost from inflation data in the country. The Stoxx 600 Real Estate Index rose as much as 6.5%, to the highest intraday since Feb., leading gains on the broader benchmark. Swedish property stocks including Fabege, Balder and Sagax were some of the top performers, getting a further boost after data showed that Sweden’s core inflation rate declined more than expected in November, increasing the possibility of interest-rate cuts. UK homebuilders — which are not part of the real estate index — also gained, with Persimmon and Taylor Wimpey both up at least 4%. Here are the top European movers:

Universal Music Group gains as much as 2.5%, rising to the highest in two years, after it was raised to buy at Citi, which said the entertainment company’s growth potential is “undervalued.”

Vivendi shares gain as much as 12% after the media conglomerate said it’s exploring splitting up into “several entities,” each of which would be listed publicly.

RWE, Enel and SSE rise as JPMorgan names them as top picks, while renewables outperform broadly on the prospect of interest rate cuts next year. Beaten-down renewable energy stocks should re-rate in 2024, JPMorgan predicts.

European real estate stocks jumped after the Fed signaled a series of interest rate cuts next year, while Swedish property shares also got a boost from inflation data in the country.

Entain rises as much as 8.1% after Corvex bought a stake representing about 4.4% of the gambling company’s outstanding shares, according to a statement.

AMS-Osram soars as much as 13%, one of the best performers on the Stoxx Europe 600, after it was upgraded to buy at Jefferies, following the recent rights issue and debt raise. The broker cites a healthy balance sheet and an industry upcycle ahead.

Brunello Cucinelli gains as much as 7.7% after the Italian luxury goods company highlighted strong sales over recent months and “excellent” order intake for its SS24 collections. There could be scope for margin upside, analysts at Deutsche Bank said.

Gold mining stocks including Fresnillo and Centamin follow the price of gold higher after the US Federal Reserve signaled its tightening campaign has ended.

Corbion shares rise as much as 6.5% after Inclusive Capital Partners Founder Jeffrey Ubben urged the company to seek strategic alternatives given the “malaise, concern, and apathy” among its public shareholders, according to statement.

Italian banks such as BPER Banca, Unicredit and Banco BPM and Spanish lenders including Sabadell and Caixabank decline after the Federal Reserve held interest rates steady and forecast a series of cuts next year.

LPP shares drop as much as 5.4%, the most since September, after Poland’s biggest fashion retailer cut its FY2023/24 sales target. Erste called the outlook conservative, which could dampen sentiment to the stock.

MorphoSys shares slide 4.6%, paring an earlier 9.6% drop%, after the German biotech firm sold €102.7 million of stock to support its pipeline development, strengthen its finances and for general corporate purposes.

Earlier in the session, Asian stocks rose to a three-month high after the Federal Reserve greenlighted interest-rate cuts for next year, reigniting a bullish pulse across markets as inflation eases. The MSCI Asia Pacific Index rose 1.6%, with AIA Group, Samsung and TSMC among the biggest boosts. Key gauges rose more than 1% in Hong Kong, South Korea and Australia. Japanese equities fell as the yen strengthened, with investors eying an eventual end to the nation’s negative rates.

Hang Seng and Shanghai Comp were initially positive with the former underpinned after the HKMA kept rates unchanged in lockstep with the Fed, while gains in the mainland were limited following the latest Chinese loans and aggregate financing data which missed estimates.

Australia’s ASX 200 was lifted with gains led by the rate-sensitive sectors after a fall in yields and with participants also digesting the latest jobs data which showed a much larger-than-expected increase in headline employment change.

Japan’s Nikkei 225 bucked the trend and was initially boosted at the open but then failed to sustain the 33,000 level and wiped out all its gains amid selling in the banking sector and headwinds from a stronger currency.

Stocks in India rallied to a new peak on Thursday, tracking gains across global markets after the Federal Reserve signaled the possibility of rate cuts next year. The S&P BSE Sensex Index rose 1.2% to 70,433 as of 10:16 a.m. Mumbai time, while the NSE Nifty 50 Index advanced 1%. The gauges still trailed MSCI’s gauge of Asian stocks which rose as much as 1.7%, its biggest gain in a month.

In FX, the dollar dropped to a four-month low, continuing its losses from Wednesday. The yen climbed by more than 1%, with the Bank of Japan tipped to be a policy outlier by scrapping the world’s last negative interest rate. The Norwegian krone sits atop the G-10 intraday rankings, rising 2% versus the greenback after the Norges Bank surprised most economists with a 25bp hike. The Swiss franc is up 0.1% after the Swiss National Bank stood pat on rates and dropped a reference to selling foreign currency.

In rates, treasuries extended the sharp rally that followed the Fed meeting, with the 10-year yield falling below 4% for the first time since August, and trading at 3.94% at last check. Yields on the policy-sensitive two-year note fell 11 basis dropping as low as 4.28% into the rally; US 2s10s, 5s30s spreads are steeper by 4bp and 5bp on the day. Traders are pricing in 161bps and 125bps of rate cuts by the end of 2024 for the ECB and BOE respectively,ahead of policy announcements at 7am (BOE) and 8:15am (ECB) New York time. Dollar IG issuance slate empty so far; most syndicate desks are of the view that primary market sales are finished for 2023; no deals were priced Wednesday ahead of the Fed.

In commodities, oil advanced from a five-month Thursday low on positive demand signals including a drop in US inventories and the potential for rate cuts by the Fed. Spot gold adds 0.3%, trading just shy of $2,040 as the global liquidity spigots are about to go full blast again.

Looking to the day ahead now, US economic data includes November retail sales, import/export price index and initial jobless claims (8:30am) and October business inventories (10am). Fed members speaker scheduled empty until Dec. 19 with Bostic speaking on the economy and business outlook at the Harvard Business School Club of Atlanta Alumni Leadership Lunch.

Market Snapshot

S&P 500 futures up 0.2% to 4,716.50

MXAP up 1.6% to 163.98

MXAPJ up 1.8% to 509.57

Nikkei down 0.7% to 32,686.25

Topix down 1.4% to 2,321.35

Hang Seng Index up 1.1% to 16,402.19

Shanghai Composite down 0.3% to 2,958.99

Sensex up 1.3% to 70,474.76

Australia S&P/ASX 200 up 1.7% to 7,377.86

Kospi up 1.3% to 2,544.18

STOXX Europe 600 up 1.3% to 478.74

German 10Y yield little changed at 2.03%

Euro up 0.3% to $1.0907

Brent Futures up 1.5% to $75.36/bbl

Gold spot up 0.5% to $2,036.91

U.S. Dollar Index down 0.31% to 102.55

Top Overnight News

Japan’s political scandal looks set to wipe out heavyweights of the ruling party’s once-mighty faction favoring big monetary stimulus, easing the path for the BOJ in pulling the economy out of decades of ultra-low interest rates. Prime Minister Fumio Kishida on Wednesday announced he would make changes to his cabinet as he seeks to stem the fallout from a fundraising scandal that has further dented public support for his embattled administration. RTRS

There are many good reasons for domestic and international investors to keep shunning Chinese stocks. Yet it is also relatively easy to be underweight a market that is underperforming. Any revival would force investors to revisit their assumptions. For those with a stomach for a high-risk, high-return trade, there is scope for a long march upwards. RTRS

The US, the UK and France are exploring ways to convince Hizbollah to pull back from the Lebanon-Israel border in a diplomatic push to prevent a full-blown conflict erupting between the militant group and Israel. FT

Norway’s Norges Bank surprises markets with a 25bp hike (from 4.25% to 4.5%) and says rates will be kept at this level “for some time”. RTRS

ECB: Given our revised inflation profile, we expect the first rate cut in April and now look for faster cuts of 25bp per meeting (vs 25bp per quarter before) until the deposit rate reaches 2.25% by early 2025. While it is possible that the Council cuts rates with the new projections in March, we view April as somewhat more likely given our expectation for firmer growth, the ongoing strength in wage growth and more data to confirm the slowdown in underlying inflation. GIR

BOE: We remain comfortable with the view that the BoE will cut policy rates later than the ECB and expect the first 25bp cut with the MPR in August. But we now see a faster pace of cuts once policy normalisation starts, with 25bp moves per meeting (vs per quarter before) until Bank Rate falls back to 3% in mid-2025. This quicker pace is more in line with historical cutting cycles, our updated forecast for the ECB and our forecast for a quicker decline in inflation. GIR

Donald Trump pulled ahead of Joe Biden in Michigan in a Bloomberg News/Morning Consult poll conducted Nov. 27-Dec. 5, after ties in October and early November. He now leads in the monthly tracking poll of all seven swing states that will decide the presidential election. BBG

Oil demand set to soften according to the IEA’s Dec report – “Global 4Q23 demand growth has been revised down by almost 400 kb/d, with Europe making up more than half the decline. The slowdown is set to continue in 2024, with global gains halving to 1.1 mb/d, as GDP growth stays below trend in major economies. Efficiency improvements and a booming electric vehicle fleet also drag on demand” IEA

Washington is nearing a breakthrough agreement on immigration reform that would clear the way for an additional package of aid for Ukraine. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher with sentiment underpinned in reaction to the FOMC.ASX 200 was lifted with gains led by the rate-sensitive sectors after a fall in yields and with participants also digesting the latest jobs data which showed a much larger-than-expected increase in headline employment change. Nikkei 225 bucked the trend and was initially boosted at the open but then failed to sustain the 33,000 level and wiped out all its gains amid selling in the banking sector and headwinds from a stronger currency. Hang Seng and Shanghai Comp were initially positive with the former underpinned after the HKMA kept rates unchanged in lockstep with the Fed, while gains in the mainland were limited following the latest Chinese loans and aggregate financing data which missed estimates.

Top Asian News

HKMA kept its base rate unchanged at 5.75%, as expected.

Japan’s negative rate exit scenario is said to be muddled by the Fed outlook with the BoJ preparing to tighten monetary policy as other central banks signal loosening, according to Nikkei.

Japan’s ruling LDP tax reform panel agreed on income tax breaks aimed at offsetting the impact of price increases on households, according to Reuters.

Chinese Commerce Ministry says external demand shows signs of warming up

Fitch Ratings says “Australia’s continued revenue outperformance and prudent fiscal management, with the government saving most of its revenue windfall, remain supportive of its ‘AAA’/Stable sovereign rating”

China’s Beijing government says it is to reduce the minimum down payment for new mortgages; payment ratio will be lowered to 30%

European equities, Eurostoxx50 (+0.7%), are firmer with clear outperformance in the FTSE 100 (+2.0%) benefitting from gains in Basic Resources.European sectors are entirely in the green with the exception of Insurance; sectoral performance today is guided by lower interest rate expectations, which has led Real Estate to the top of the pile. US equity futures are trading higher after a dovish FOMC policy announcement on Wednesday, where the US central bank signalled that three 25bps rate cuts were coming in 2024; the RTY (+0.9%) outperforms after soaring 3.5% yesterday.

Top European News

German DIW lowers domestic growth forecasts. 2024: 0.6% (prev. 1.2%), 2025 1.0% (prev. 1.2%)

Germany’s IFO lowers its 2024 GDP growth forecast to 0.9% from +1.4% previously; upgrades 2025 to +1.3% from +1.2%

Around 65% of EV cars sold in France will be eligible for a new state bonus scheme, via Reuters citing sources

Central Banks: SNB

Maintains its Policy Rate at 1.75% as expected; prepared to be active in the FX market as necessary (removed reference to “selling”)

Will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term. (Prev. “it cannot be ruled out that a further tightening of monetary policy may become necessary to ensure price stability over the medium term.”)

Click here for more details.

SNB Chairman Press Conference: SNB is no longer focussed on selling FX. This reflects that monetary conditions are currently appropriate; does not forecast any tightening given the forecasts so far; rate cuts were not part of the discussion today.

Central Banks: Norges Bank:

Unexpectedly hikes its Key Policy Rate to 4.50% from 4.25% (exp. a hold at 4.25%); The forecast indicates that the policy rate will lie around 4.5% until autumn 2024 before gradually moving down

The policy rate is likely close to the level required to return inflation to target within a reasonable time horizon. On the other hand, inflation is high, and the krone depreciation makes it more challenging to bring down inflation.

If cost inflation remains elevated or the krone turns out to be weaker than projected, price inflation may remain higher for longer than currently projected. In that case, the Committee is prepared to raise the policy rate again.

If there is a more pronounced slowdown in the Norwegian economy or inflation declines more rapidly, the policy rate may be lowered earlier than currently envisaged.

FX

A subdued morning for the broader Dollar and index in a continuation of the losses seen after markets were surprised by the extent of the Powell pivot.

The Sterling and EUR modestly gain against the USD compared to some G10 peers are participants look ahead to the BoE and EUR confabs.

JPY is the top gainer in the European morning amid the hefty fall in the Dollar and US yields.

AUD, NZD, CAD are among the top gainers following the boost to risk sentiment and the Fed-induced surge in commodity prices.

EUR/CHF initially immediately moved lower (following the SNB) from 0.9499 to 0.9460 before recoiling back to highs of 0.9518 and then stabilising just under pre-announcement levels around 0.9492.

A hike at the Norges Bank sparked marked NOK appreciation against both the EUR and USD. USD/NOK fell from 10.70 to 10.60 before falling to a 10.5860 trough.

PBoC set USD/CNY mid-point at 7.1090 vs exp. 7.1566 (prev. 7.1126).

Fixed Income

USTs are comparably contained, given US-specific risk events have now passed, with upside of around 20 ticks having extended marginally above Wednesday’s best; 10yr yield still sub-4.0%.

Gilts have similarly trimmed from a 101.69 best but still hang on to upside in excess of 100ticks, likely given recent relative underperformance in Gilts.

Bunds are holding just below the 137.00 mark having trimmed incrementally from the initial 137.28 high as newsflow slows slightly and attention turns to Lagarde.

Commodities

WTI Jan and Brent (+2.0%) Feb futures remain on a firmer footing in a continuation of the fallout from the FOMC policy announcement and press conference, which ultimately was more dovish than expected.

Spot gold was catapulted by the demised in the Dollar and yields following the Fed statement and press conference, with the opening candle at the time at USD 1,982.35/oz; Base metals similarly surged although gains overnight were capped by the mixed APAC mood.

IEA OMR: trims 2023 global oil demand growth forecast by 90k to 2.3mln BPD; 2024 demand forecast raised by 130k to 1.1mln BPD citing improved GDP outlook

BofA expects ULSD to Brent cracks to average USD 26/bbl in 2024 (vs average USD 36/bbl this year)

Citi (C) says “COP28 momentum for renewables is super-bullish for metals demand and fossil fuel aspirations more challenging”

Geopolitics

US National Security Adviser Sullivan met with Saudi’s Crown Prince MBS and discussed the humanitarian response in Gaza including efforts to increase the flow of critical aid, according to the White House.

US is reportedly holding up the licences for selling over 20k rifles to Israel due to concerns about attacks by extremist Israeli settlers against Palestinian civilians in the West Bank, according to sources cited by Axios.

US, Japan and Philippines national security advisers held a call and expressed concerns about China’s recent dangerous and unlawful conduct in the South China Sea, according to Reuters.

Chinese Embassy in Canada said China condemns Canada’s support for the Philippines in violating China’s sovereignty in the South China Sea, according to Reuters.

Iranian Defense Minister says the US “will face major problems if it wants to form an international force in the Red Sea”, according to Al Jazeera; adds “We have control in the Red Sea and all countries are present in it and no one can manoeuvre there”

US Event Calendar

08:30: Dec. Initial Jobless Claims, est. 220,000, prior 220,000

Dec. Continuing Claims, est. 1.88m, prior 1.86m

08:30: Nov. Retail Sales Advance MoM, est. -0.1%, prior -0.1%

Nov. Retail Sales Ex Auto and Gas, est. 0.2%, prior 0.1%

Nov. Retail Sales Ex Auto MoM, est. -0.1%, prior 0.1%

Nov. Retail Sales Control Group, est. 0.2%, prior 0.2%

08:30: Nov. Import Price Index YoY, est. -2.1%, prior -2.0%

Nov. Import Price Index MoM, est. -0.8%, prior -0.8%

08:30: Nov. Export Price Index YoY, est. -5.2%, prior -4.9%

Nov. Export Price Index MoM, est. -1.0%, prior -1.1%

10:00: Oct. Business Inventories, est. -0.1%, prior 0.4%

DB’s Jim Reid concludes the overnight wrap

Yesterday’s FOMC meeting did its best to give investors an early Christmas present, all packaged with a bow and extra special gift wrapping. In turn this added more fuel to the soft landing narrative. Our 2024 outlook has 175bps of Fed cuts in it but this is premised on a mild recession. One change to a dot plot doesn’t automatically completely change the direction for the economy but the risks that the Fed stubbornly hold in restrictive territory while the lag of policy hits has been reduced by their change of tone .

Markets were very bulled up by the move and the positive market reaction to the initial decision gained further traction during Powell’s conference. By the end of the day, 2yr treasury yields were down over 30bps and the S&P 500 reached a record high in total return terms. The bond rally has extended overnight, with 10yr yields (-3.38bps) falling below 4% as I type. We’ll see if European central banks are anywhere near as festive today, with the ECB and BoE decisions due later. Don’t forget US retail sales and initial jobless claims too.

Starting with the Fed details, a dovish shift was signalled first of all by the updated SEP dot plot, with the median FOMC member moving to expect 75bps of rate cuts in 2024 (from 50bps before but from a lower peak). The number of officials seeing risks to inflation as titled to the upside also went down from 14 to 8 (out of 19), with most now seeing risks as balanced. In the statement, there were dovish tweaks on inflation and activity, while the previous hawkish bias was toned down, adding “any” in its reference to “the extent of any additional policy firming that may be appropriate”.

Powell confirmed in the press conference that participants no longer expected further hikes, although they did not want to take the possibility off the table. Further, he stated that a “preliminary” discussion around rate cuts took place at the December meeting and offered no direct pushback when asked about recent market pricing. There were one or two elements of caution in his comments, indicating that “no one is declaring victory”. But overall he struck an optimistic tone on the progress made in fighting inflation, validating a dovish risk-on takeaway. Following the FOMC, our US economists maintain the expectations of 175bps of cuts from the Fed in 2024 starting in June, but with heightened risks that rate cuts could come as early as March. See their full reaction note here.

Following the Fed, money markets moved to price earlier and more aggressive rate cuts, with fed funds futures overnight moving to fully price a 25bps cut by the March meeting (up from a 43% chance as of Tuesday and 92% at yesterday’s close). And ~150bps of rate cuts are priced by end-24 as I type, up from 110bps this time yesterday.

Bonds rallied sharply, with 2yr and 10yr treasury yields falling by c. 15bps and 10bps respectively immediately after the Fed decision, and declining further during Powell’s press conference and overnight. 2yr yields were down -30.3bps yesterday to 4.43%, their biggest daily decline since March, and are trading another -5.2bps lower overnight. Meanwhile, the 10yr closed -18.5bps lower at 4.02%, its lowest in four months. It has extended the decline to 3.98% as I type. A remarkable turnaround since the 10yr traded above 5% intra-day on October 23. The major bull steepening in US rates has provided a challenging backdrop for the dollar,with the broad dollar index down -0.96% yesterday and around another -0.28% this morning .

Equities rallied strongly on the Fed’s upbeat message. The S&P 500 had been trading near flat on the day prior to the FOMC but rose by half a percent immediately after the decision, and by a similar amount during Powell’s press conference. It was +1.37% by the close, up to its highest level in nearly two years. The bigger milestone for the S&P 500 came in total return terms, which reached a new record high (eclipsing the peak of January 2022). The year-to-date total return on the index is now +24.5%. Across sectors, tech mega caps underperformed in the broad rally (Magnificent Seven +0.64%). On the other hand, small caps strongly outperformed with the Russell 2000 (+3.52% yesterday) approaching bull market territory, having risen 19% from its trough in late October. S&P 500 (+0.38%) and NASDAQ 100 (+0.53%) futures are rising further this morning.

Looking back at yesterday prior to the Fed decision, US Treasuries had already got some momentum from a softer-than-expected PPI reading for November. In particular, t he core measure excluding food and energy was at just +0.1% (vs. +0.2% expected), which took the year-on-year measure down to +2.0% (vs. +2.2% expected), marking its lowest level since January 2021. Some of the PPI components feed into the Fed’s preferred PCE measure of inflation, so all things being equal the decline offers further support for the prospect of rate cuts next year.

Looking forward now, central banks will stay in the spotlight today, as both the ECB and the Bank of England are also announcing their latest policy decisions. For the ECB, it’s widely expected that they’ll be leaving their policy rate unchanged for a second consecutive meeting. But as with the Fed, speculation about rate cuts has mounted considerably in recent weeks, particularly after the latest inflation data showed CPI falling to 2.4% in November. At today’s press conference, our European economists expect the ECB to acknowledge this faster-than-expected decline, but to be coy about declaring victory prematurely. They think they’ll keep the guidance that maintaining restrictive rates for sufficiently long will bring inflation back to target in a timely manner, and they don’t expect the ECB to cut rates until April even if March is an increasing risk. See their full preview here.

Here in the UK, the Bank of England will also be deciding on rates, and it’s similarly expected that they’ll remain on hold. For now at least, the inflation situation in the UK remains comparatively worse than the US and the Euro Area, since CPI was still at 4.6% in October. So markets are pricing a slower pace of rate cuts from the BoE relative to the Fed and the ECB, with just 35bps of cuts priced in by the June meeting although this might change this morning. Moreover, our UK economist still expects there to be a split vote tally at the latest meeting, with 3 of the 9 members continuing to vote in favour of another 25bp hike. Looking forward, he expects rate cuts from Q2 2024, but thinks the risks of a delay are mounting. See his full preview here.

Ahead of those, European equities put in a steady performance before the Fed’s decision, with the STOXX 600 (-0.06%) posting a slight decline, just as sovereign bond yields fell to their lowest in months thanks to that US PPI reading. For instance, yields on 10yr bunds were down -5.4bps to 2.17%, and those on 10yr OATs were down -6.0bps to 2.71%. In both cases that’s their lowest level in 8 months. Moreover, gilts saw an even larger decline, with the 10yr yield down -13.5bps to 3.83%. That followed the release of monthly GDP data for the UK, which fell by -0.3% in October (vs. -0.1% expected), and led investors to become more confident about the prospect of BoE rate cuts next year. Expect to see these yields gap lower at the open after the Fed move last night.

Asian equity markets are continuing the rally this morning with the KOSPI (+1.32%) leading gains closely followed by the Hang Seng (+1.11%) while the CSI (+0.25%) and the Shanghai Composite (+0.30%) are also edging higher but with the China move subdued again. Meanwhile, the Nikkei (-0.86%) is on the weaker side reversing its initial gains as the Yen drives higher (+0.78%) to 141.77 after the FOMC .

Early morning data showed that core machine orders in Japan unexpectedly advanced +0.7% m/m in October (v/s -0.4% expected) as against an increase of +1.4% in the previous month. However, it remained down year-on-year (-2.2%) as uncertainty about the global economy pared companies’ appetite for fresh investments.

In other news yesterday, the German government reached a political agreement on how to rework the 2024 budget. Overall consolidation needs are in line with our economists’ earlier estimates (EUR 30bn), leading to a tighter fiscal stance for 2024 and slightly higher inflation. A loophole for a potential suspension of the debt brake in case of higher Ukraine support has been left open. See our Germany economists’ report here for details.

To the day ahead now, and the main highlights will be the monetary policy decisions from the ECB and the Bank of England. Otherwise, US data releases include the weekly initial jobless claims and retail sales for November.

Tyler Durden

Thu, 12/14/2023 – 08:08