Expect Fed To Maintain ‘Higher For Longer’ With Steeper Dots Curve

Authored by Simon White, Bloomberg macro strategist,

Market expectations of interest rate cuts are unlikely to be endorsed by the Federal Reserve’s dot plot today.

The totality of its Summary of Economic Projections should maintain the higher-for-longer message and thus, as it is no overall change, be fairly neutral for the bond and money markets once the dust has settled.

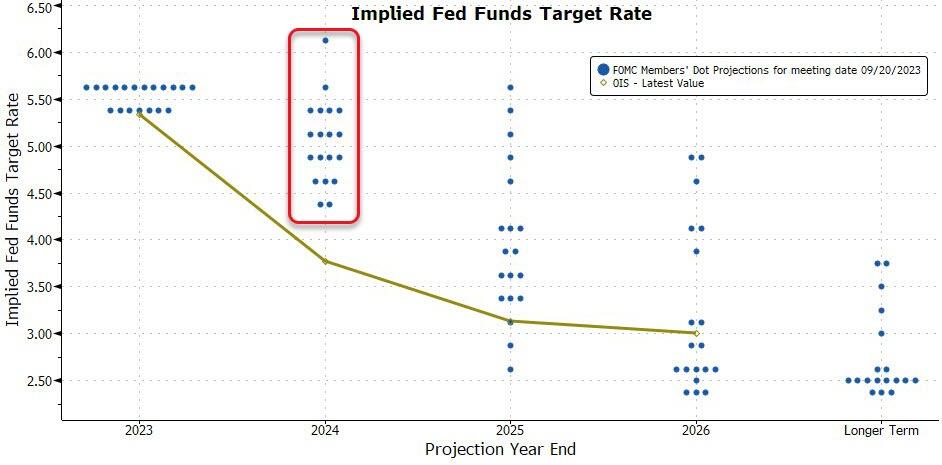

Another central-bank bonanza is upon us, and the parlor game of scrutinizing policymakers’ every utterance or non-utterance can get going again in earnest. The Fed has added a whole new dimension to the game with the SEP, allowing every FOMC member to make anonymous forecasts for where fed funds, growth, inflation and the unemployment rate will be in the coming years.

The market has been gunning for increasingly larger rate cuts next year, with 110 bps now priced.That’s getting into “hard-landing” territory, and there’s not enough evidence today to support that notion with such a high degree of certainty – definitely not to the point that the Fed will want to squander its tightening work up until now.

{kind=link}

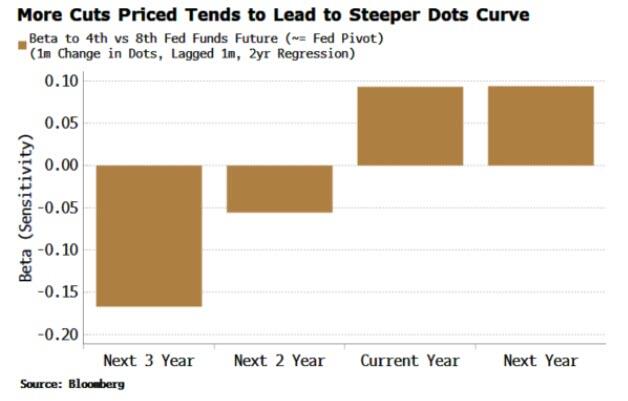

When the market increases the amount of cuts it is expecting (the Fed “pivot”), that has tended to elicit a steepening of the dots curve by the FOMC.

The chart below shows the sensitivity of each dot to the 4th vs 8th fed funds future contracts (~= to the Fed pivot) lagged by one month.Thus when the fed fund curve flattens the two and three-year dots will tend to be marked up and the nearer-term dots be marked down, i.e. the FOMC leans against the market’s flattening by steepening the dots curve.

{kind=link}

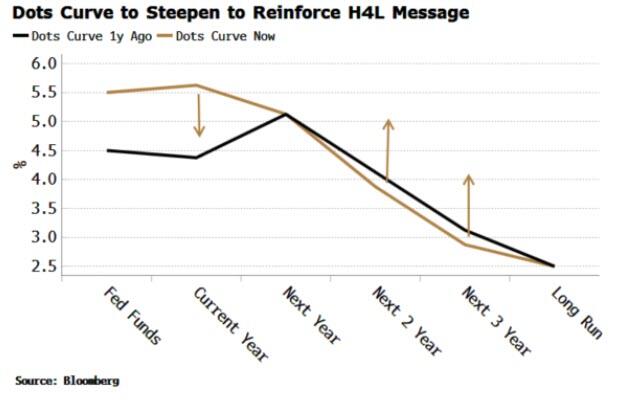

As the fed funds curve has flattened over the last month, a similar FOMC reaction function should result in a steeper dots curve at today’s meeting.

That would mean it heading back in the same direction of where it was a year ago, when spot rates were lower but the Fed was forecasting slightly higher rates further out.

{kind=link}

This will reinforce the higher-for-longer message, while the Fed can use the other forecasts in the SEP to convey the message that economy is slowing, and some rate cuts could be forthcoming if inflation does not reignite.

Explicitly, they will likely use the SEP to mark down their growth forecasts and mark up their unemployment ones. They may also mark down their inflation forecasts, but if they do then it’s unlikely to be by much as this would send out the wrong signal(plus the tick up in supercore CPI after Tuesday’s CPI release is likely to temper any premature inflation optimism).

ZH: Finally, we note that Goldman’s Mike Cahill believes:

“there is a possibility that we end up with a situation like early 2022 where central banks initially moved more slowly than the market, but ultimately the market had a better handle on the direction than policymakers.

For the Fed right now, the market needs clarity on the reaction function – was Waller speaking for the Committee when he gave his framework for cuts?

The combination of the dots + economic projections will help with that, and in my view that combination, and subsequent commentary from Fed officials, will be more useful than the exact number of cuts written into the forecast, especially because we have a stronger growth outlook (with less rates support) than most.”

Cahill is likely right – the market bossing The Fed – but the end result will be Arthur Burns-ian… and that’s not what Powell wants his legacy to be.

Tyler Durden

Wed, 12/13/2023 – 09:40