It’s Dark, But Breadth Says It’s Not Quite Dawn For China Stocks

Authored by Simon White, Bloomberg macro strategist,

After another dismal set of China inflation data, sentiment for Chinese stocks feels like it can’t get much worse.

That can be a sign the market will soon bottom, but breadth is not yet at the extreme capitulatory levels that would give a much higher confidence to this view. Nevertheless, the risk-reward for some exposure to China stocks remains attractive.

I had thought the bottom in China stock was perhaps in last month, but the economic data has continued to be dreadful. Over the weekend, November’s CPI came in at -0.5% and PPI at -3%, both lower than the previous month.

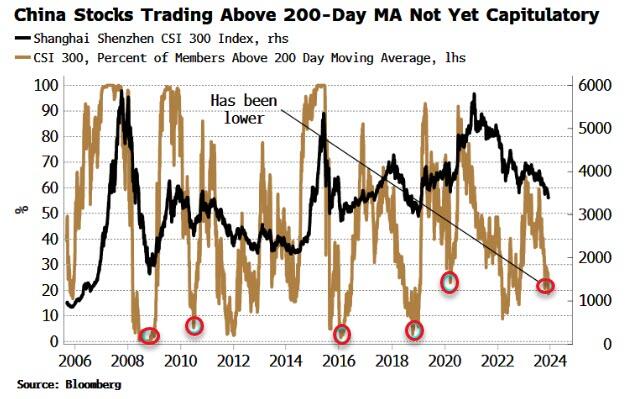

Confidence would be higher that a tradeable bottom is near if breadth was more extreme. However, the net number of stocks in the CSI 300 index making new 52-week lows has been more stretched at previous bottoms in the index. Similarly for the number of stocks with an RSI of less than 30 and the percentage of stocks trading below their 200-day moving averages.

Furthermore, we haven’t yet seen a spike in volume which often occurs at capitulatory junctures.

{kind=link}

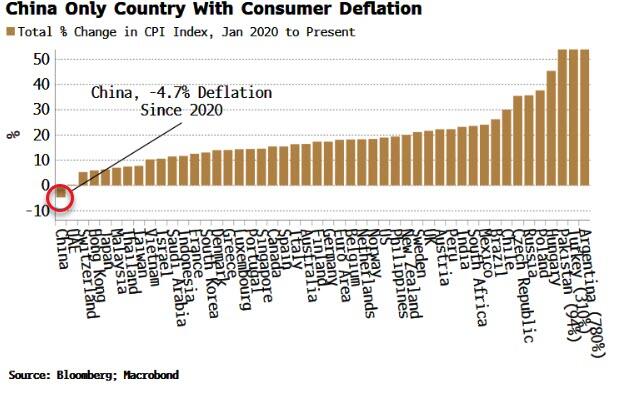

China’s decision to have one of the longest and most stringent lockdowns while giving its household sector scant support (unlike many DM countries) has led to the country being the only one to have experienced outright deflation since 2020, when every other main country has experienced inflation, often the highest for decades.

{kind=link}

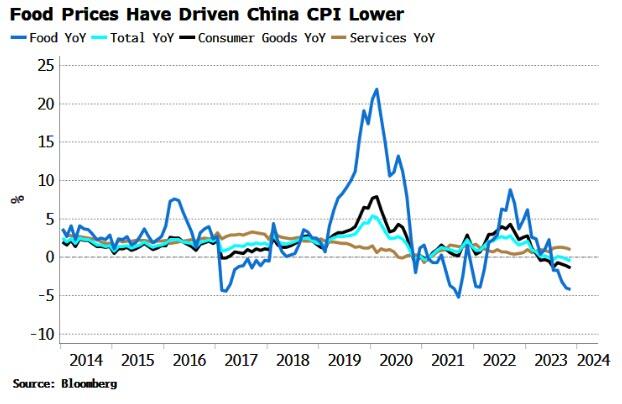

A weak real-estate sector and the severe dent to confidence from lockdowns has led to a spend-averse household sector.

The fall in CPI is being driven by a decline in food and consumer goods. Food is estimated to be about a third of the CPI basket, with goods (including food) accounting for just under two thirds of the total.

Global food prices have started to rise again, so this may soon provide support to China’s CPI.

{kind=link}

With so much bad news already in the price, there is good risk-reward for beginning to accumulate China stocks, but breadth data suggests we are perhaps not quite yet at the point of “revulsion,”forcing the last speculative longs out, and clearing the way for a sustainable rally.

Tyler Durden

Mon, 12/11/2023 – 17:00